FHA Loan Limits in Indiana: Mortgage Guidelines 2024

Applying for an FHA loan can be a long and confusing process. You have to gather all of your financial information, know your Indiana FHA Loan limits, submit it to the lender, and then wait to hear back. We are an online resource that connects you with FHA-approved lenders in Indiana so that you can get pre-approved for an FHA loan fast. Plus, our lenders offer competitive rates and terms so that you can find the best mortgage for your needs.

Applying for an FHA loan can be a long and confusing process. You have to gather all of your financial information, know your Indiana FHA Loan limits, submit it to the lender, and then wait to hear back. We are an online resource that connects you with FHA-approved lenders in Indiana so that you can get pre-approved for an FHA loan fast. Plus, our lenders offer competitive rates and terms so that you can find the best mortgage for your needs.

What are FHA Loan Limits 2024?

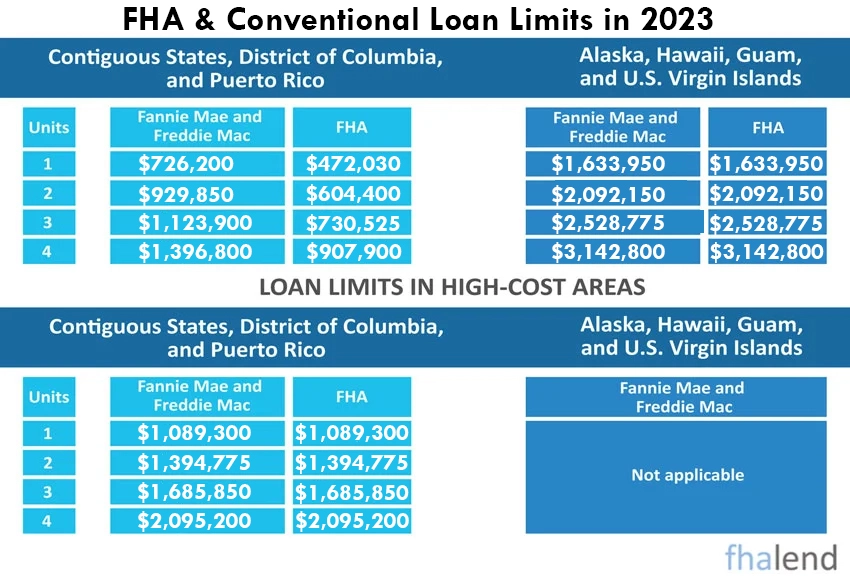

The Federal Housing Administration, or FHA, was created to assist low- and moderate-income homebuyers in obtaining mortgage loans. The FHA sets yearly FHA loan limits for buyers who take out FHA loans (any bank or mortgage company insured or guaranteed by the FHA) and those limits are based on the area’s average house price. The higher the loan limit, the more expensive the typical house.

The limit is based on the area’s median home price, which is set at 115% of that figure in low-cost locales and 150% in high-cost locations. The FHA adjusts loan limits each year based on the most up-to-date sales data available. With home prices, the FHA mortgage loan limits fluctuate. This is to ensure that people in high-cost regions have the opportunity to acquire a loan that will allow them to access an expensive market.

FHA Loan Indiana Requirements:

- Job History – Stable income and employment. Proof of employment for 2 years is required. It is ok if you have changed jobs, but you need to show consistent employment/income. People with a part-time income need to be seasoned for at least 2 years.

- Financial Statements – You should expect to be required to provide your 2 most recent bank statements, pay stubs, and tax returns.

- Credit Score – To qualify for the FHA loan you must have a 500 credit score or higher.

- Down Payment – HUD requires a 3,5% down payment for the FHA Loan depending on your credit score. On $300,000 house you will need $10,500. If your credit score is between 500–579, you are eligible for up to 90% financing. So the minimum down payment would be 10% of your home’s purchasing price. So if you buy a house worth $300.000 you need to come up with $30,000.

- Debt-to-Income (DTI) – You can not have a debt-to-income ratio higher than 43%. However, if you have “compensating factors” you might be able to get approved with higher debt levels (a compensating factor could be more money in savings, long job history, or great credit).

- Primary Residence – You must occupy the home that you intend to purchase and have it be your primary residence. FHA loans are not available to purchase an investment property, second home, or vacation home. It’s possible to add a non-occupying co-borrower to the FHA mortgage loan also.

- Mortgage Insurance – All FHA loans, regardless of the lender, require two types of mortgage insurance. This includes the UPMIP (Upfront Mortgage Insurance Premium) and the regular MIP (Mortgage Insurance Premium). FHA MIP acts similarly to how PMI (Private Mortgage Insurance) on a conventional loan acts. You can use our loan calculator to estimate your monthly payment and mortgage insurance costs.

- FHA Loan Limits (Maximum FHA loan amount) – FHA loans have maximum lending limits, which are set at the county level. You can view the 2024 FHA loan limits for all counties in Indiana below.

We know that you’re busy and you don’t want to waste your time talking to a bunch of lenders who won’t give you the time of day. At FHA Lend we do loans in Indiana, we’ll do the work for you. We have a wide network of approved lenders who are ready to help you get into your dream home. Request a free consultation today and one of our friendly loan officers will be happy to help.

Indiana FHA Loan Limits by County in 2024

In 2024, in Indiana FHA loan limits are up to $472,030will be available for a one-unit property. The FHA limit for a two-unit home is $604,400. For a three-unit home it’s $730,525. A four-unit home is the FHA limit of $907,900. In High-cost areas limits are follow: $970,800 for Single Unit, for Duplexes: $1,243,050, for Triplexes (three units) is $1,502,475 and for Four units is $1,867,275.

| County | FHA Limit | 2 Family | 3 Family | 4 Family | FHFA limit | Median House Price |

|---|---|---|---|---|---|---|

| DILLINGHAM CENS | $498,257 | $637,950 | $771,125 | $958,350 | $209,000 | $323.7 |

| HAINES BOROUGH | $498,257 | $637,950 | $771,125 | $958,350 | $282,000 | $323.7 |

| KENAI PENINSULA | $498,257 | $637,950 | $771,125 | $958,350 | $294,000 | $323.7 |

| LAKE AND PENINS | $498,257 | $637,950 | $771,125 | $958,350 | $156,000 | $323.7 |

| PRINCE OF WALES | $498,257 | $637,950 | $771,125 | $958,350 | $258,000 | $323.7 |

| BALDWIN | $498,257 | $637,950 | $771,125 | $958,350 | $295,000 | $323.7 |

| COVINGTON | $498,257 | $637,950 | $771,125 | $958,350 | $100,000 | $323.7 |

| FRANKLIN | $498,257 | $637,950 | $771,125 | $958,350 | $97,000 | $323.7 |

| WASHINGTON | $498,257 | $637,950 | $771,125 | $958,350 | $157,000 | $323.7 |

| WINSTON | $498,257 | $637,950 | $771,125 | $958,350 | $100,000 | $323.7 |

| FRANKLIN | $498,257 | $637,950 | $771,125 | $958,350 | $155,000 | $323.7 |

| HOT SPRING | $498,257 | $637,950 | $771,125 | $958,350 | $120,000 | $323.7 |

| INDEPENDENCE | $498,257 | $637,950 | $771,125 | $958,350 | $115,000 | $323.7 |

| LINCOLN | $498,257 | $637,950 | $771,125 | $958,350 | $138,000 | $323.7 |

| POINSETT | $498,257 | $637,950 | $771,125 | $958,350 | $190,000 | $323.7 |

| SALINE | $498,257 | $637,950 | $771,125 | $958,350 | $214,000 | $323.7 |

| WASHINGTON | $498,257 | $637,950 | $771,125 | $958,350 | $336,000 | $323.7 |

| SWAINS ISLAND | $498,257 | $637,950 | $771,125 | $958,350 | $122,000 | $323.7 |

| COCONINO | $525,550 | $672,800 | $813,250 | $1,010,700 | $457,000 | $341.25 |

| PINAL | $530,150 | $678,700 | $820,350 | $1,019,550 | $460,000 | $344.5 |

| ALPINE | $503,700 | $644,800 | $779,450 | $968,650 | $438,000 | $326.95 |

| INYO | $508,300 | $650,700 | $786,550 | $977,500 | $400,000 | $330.2 |

| KINGS | $498,257 | $637,950 | $771,125 | $958,350 | $337,000 | $323.7 |

| MARIN | $1,149,825 | $1,472,250 | $1,779,525 | $2,211,600 | $595,000 | $0.65 |

| MENDOCINO | $546,250 | $699,300 | $845,300 | $1,050,500 | $428,000 | $354.9 |

| SAN BERNARDINO | $644,000 | $824,450 | $996,550 | $1,238,500 | $557,000 | $418.6 |

| SAN JOAQUIN | $656,650 | $840,650 | $1,016,150 | $1,262,800 | $565,000 | $426.4 |

| TRINITY | $498,257 | $637,950 | $771,125 | $958,350 | $185,000 | $323.7 |

| GILPIN | $816,500 | $1,045,250 | $1,263,500 | $1,570,200 | $710,000 | $530.4 |

| HINSDALE | $498,257 | $637,950 | $771,125 | $958,350 | $345,000 | $323.7 |

| LINCOLN | $498,257 | $637,950 | $771,125 | $958,350 | $173,000 | $323.7 |

| MINERAL | $498,257 | $637,950 | $771,125 | $958,350 | $252,000 | $323.7 |

| PITKIN | $1,149,825 | $1,472,250 | $1,779,525 | $2,211,600 | $50,000 | $0.65 |

| WASHINGTON | $498,257 | $637,950 | $771,125 | $958,350 | $150,000 | $323.7 |

| WINDHAM | $498,257 | $637,950 | $771,125 | $958,350 | $420,000 | $323.7 |

| FRANKLIN | $498,257 | $637,950 | $771,125 | $958,350 | $166,000 | $323.7 |

| INDIAN RIVER | $498,257 | $637,950 | $771,125 | $958,350 | $366,000 | $323.7 |

| MARTIN | $546,250 | $699,300 | $845,300 | $1,050,500 | $475,000 | $354.9 |

| PINELLAS | $498,257 | $637,950 | $771,125 | $958,350 | $400,000 | $323.7 |

| SEMINOLE | $498,257 | $637,950 | $771,125 | $958,350 | $426,000 | $323.7 |

| WASHINGTON | $498,257 | $637,950 | $771,125 | $958,350 | $119,000 | $323.7 |

| APPLING | $498,257 | $637,950 | $771,125 | $958,350 | $70,000 | $323.7 |

| ATKINSON | $498,257 | $637,950 | $771,125 | $958,350 | $84,000 | $323.7 |

| BALDWIN | $498,257 | $637,950 | $771,125 | $958,350 | $150,000 | $323.7 |

| CLINCH | $498,257 | $637,950 | $771,125 | $958,350 | $69,000 | $323.7 |

| EFFINGHAM | $498,257 | $637,950 | $771,125 | $958,350 | $365,000 | $323.7 |

| FANNIN | $498,257 | $637,950 | $771,125 | $958,350 | $365,000 | $323.7 |

| FRANKLIN | $498,257 | $637,950 | $771,125 | $958,350 | $170,000 | $323.7 |

| GWINNETT | $649,750 | $831,800 | $1,005,450 | $1,249,550 | $565,000 | $421.85 |

| IRWIN | $498,257 | $637,950 | $771,125 | $958,350 | $59,000 | $323.7 |

| JENKINS | $498,257 | $637,950 | $771,125 | $958,350 | $63,000 | $323.7 |

| LINCOLN | $498,257 | $637,950 | $771,125 | $958,350 | $297,000 | $323.7 |

| LUMPKIN | $498,257 | $637,950 | $771,125 | $958,350 | $280,000 | $323.7 |

| MCINTOSH | $498,257 | $637,950 | $771,125 | $958,350 | $300,000 | $323.7 |

| PAULDING | $649,750 | $831,800 | $1,005,450 | $1,249,550 | $565,000 | $421.85 |

| SEMINOLE | $498,257 | $637,950 | $771,125 | $958,350 | $70,000 | $323.7 |

| SPALDING | $649,750 | $831,800 | $1,005,450 | $1,249,550 | $565,000 | $421.85 |

| WASHINGTON | $498,257 | $637,950 | $771,125 | $958,350 | $80,000 | $323.7 |

| WILKINSON | $498,257 | $637,950 | $771,125 | $958,350 | $50,000 | $323.7 |

| CLINTON | $498,257 | $637,950 | $771,125 | $958,350 | $118,000 | $323.7 |

| DES MOINES | $498,257 | $637,950 | $771,125 | $958,350 | $188,000 | $323.7 |

| DICKINSON | $498,257 | $637,950 | $771,125 | $958,350 | $290,000 | $323.7 |

| FRANKLIN | $498,257 | $637,950 | $771,125 | $958,350 | $78,000 | $323.7 |

| HARDIN | $498,257 | $637,950 | $771,125 | $958,350 | $98,000 | $323.7 |

| LINN | $498,257 | $637,950 | $771,125 | $958,350 | $187,000 | $323.7 |

| MUSCATINE | $498,257 | $637,950 | $771,125 | $958,350 | $153,000 | $323.7 |

| RINGGOLD | $498,257 | $637,950 | $771,125 | $958,350 | $90,000 | $323.7 |

| WASHINGTON | $498,257 | $637,950 | $771,125 | $958,350 | $315,000 | $323.7 |

| WINNEBAGO | $498,257 | $637,950 | $771,125 | $958,350 | $122,000 | $323.7 |

| WINNESHIEK | $498,257 | $637,950 | $771,125 | $958,350 | $178,000 | $323.7 |

| BINGHAM | $498,257 | $637,950 | $771,125 | $958,350 | $315,000 | $323.7 |

| BLAINE | $759,000 | $971,650 | $1,174,500 | $1,459,650 | $660,000 | $493.35 |

| FRANKLIN | $498,257 | $637,950 | $771,125 | $958,350 | $430,000 | $323.7 |

| GOODING | $498,257 | $637,950 | $771,125 | $958,350 | $266,000 | $323.7 |

| LINCOLN | $498,257 | $637,950 | $771,125 | $958,350 | $263,000 | $323.7 |

| MINIDOKA | $498,257 | $637,950 | $771,125 | $958,350 | $302,000 | $323.7 |

| TWIN FALLS | $498,257 | $637,950 | $771,125 | $958,350 | $322,000 | $323.7 |

| WASHINGTON | $498,257 | $637,950 | $771,125 | $958,350 | $250,000 | $323.7 |

| ADAMS | $498,257 | $637,950 | $771,125 | $958,350 | $137,000 | $323.7 |

| ALEXANDER | $498,257 | $637,950 | $771,125 | $958,350 | $205,000 | $323.7 |

| BOND | $498,257 | $637,950 | $771,125 | $958,350 | $350,000 | $323.7 |

| BOONE | $498,257 | $637,950 | $771,125 | $958,350 | $206,000 | $323.7 |

| BROWN | $498,257 | $637,950 | $771,125 | $958,350 | $73,000 | $323.7 |

| BUREAU | $498,257 | $637,950 | $771,125 | $958,350 | $320,000 | $323.7 |

| CALHOUN | $498,257 | $637,950 | $771,125 | $958,350 | $350,000 | $323.7 |

| CARROLL | $498,257 | $637,950 | $771,125 | $958,350 | $87,000 | $323.7 |

| CASS | $498,257 | $637,950 | $771,125 | $958,350 | $70,000 | $323.7 |

| CHAMPAIGN | $498,257 | $637,950 | $771,125 | $958,350 | $190,000 | $323.7 |

| CHRISTIAN | $498,257 | $637,950 | $771,125 | $958,350 | $83,000 | $323.7 |

| CLARK | $498,257 | $637,950 | $771,125 | $958,350 | $87,000 | $323.7 |

| CLAY | $498,257 | $637,950 | $771,125 | $958,350 | $77,000 | $323.7 |

| CLINTON | $498,257 | $637,950 | $771,125 | $958,350 | $350,000 | $323.7 |

| COLES | $498,257 | $637,950 | $771,125 | $958,350 | $120,000 | $323.7 |

| COOK | $498,257 | $637,950 | $771,125 | $958,350 | $400,000 | $323.7 |

| CRAWFORD | $498,257 | $637,950 | $771,125 | $958,350 | $82,000 | $323.7 |

| CUMBERLAND | $498,257 | $637,950 | $771,125 | $958,350 | $120,000 | $323.7 |

| DEKALB | $498,257 | $637,950 | $771,125 | $958,350 | $400,000 | $323.7 |

| DE WITT | $498,257 | $637,950 | $771,125 | $958,350 | $91,000 | $323.7 |

| DOUGLAS | $498,257 | $637,950 | $771,125 | $958,350 | $95,000 | $323.7 |

| DUPAGE | $498,257 | $637,950 | $771,125 | $958,350 | $400,000 | $323.7 |

| EDGAR | $498,257 | $637,950 | $771,125 | $958,350 | $49,000 | $323.7 |

| EDWARDS | $498,257 | $637,950 | $771,125 | $958,350 | $60,000 | $323.7 |

| EFFINGHAM | $498,257 | $637,950 | $771,125 | $958,350 | $135,000 | $323.7 |

| FAYETTE | $498,257 | $637,950 | $771,125 | $958,350 | $78,000 | $323.7 |

| FORD | $498,257 | $637,950 | $771,125 | $958,350 | $107,000 | $323.7 |

| FRANKLIN | $498,257 | $637,950 | $771,125 | $958,350 | $101,000 | $323.7 |

| FULTON | $498,257 | $637,950 | $771,125 | $958,350 | $150,000 | $323.7 |

| GALLATIN | $498,257 | $637,950 | $771,125 | $958,350 | $74,000 | $323.7 |

| GREENE | $498,257 | $637,950 | $771,125 | $958,350 | $108,000 | $323.7 |

| GRUNDY | $498,257 | $637,950 | $771,125 | $958,350 | $400,000 | $323.7 |

| HAMILTON | $498,257 | $637,950 | $771,125 | $958,350 | $40,000 | $323.7 |

| HANCOCK | $498,257 | $637,950 | $771,125 | $958,350 | $113,000 | $323.7 |

| HARDIN | $498,257 | $637,950 | $771,125 | $958,350 | $33,000 | $323.7 |

| HENDERSON | $498,257 | $637,950 | $771,125 | $958,350 | $188,000 | $323.7 |

| HENRY | $498,257 | $637,950 | $771,125 | $958,350 | $195,000 | $323.7 |

| IROQUOIS | $498,257 | $637,950 | $771,125 | $958,350 | $103,000 | $323.7 |

| JACKSON | $498,257 | $637,950 | $771,125 | $958,350 | $146,000 | $323.7 |

| JASPER | $498,257 | $637,950 | $771,125 | $958,350 | $79,000 | $323.7 |

| JEFFERSON | $498,257 | $637,950 | $771,125 | $958,350 | $90,000 | $323.7 |

| JERSEY | $498,257 | $637,950 | $771,125 | $958,350 | $350,000 | $323.7 |

| JO DAVIESS | $498,257 | $637,950 | $771,125 | $958,350 | $200,000 | $323.7 |

| JOHNSON | $498,257 | $637,950 | $771,125 | $958,350 | $146,000 | $323.7 |

| KANE | $498,257 | $637,950 | $771,125 | $958,350 | $400,000 | $323.7 |

| KANKAKEE | $498,257 | $637,950 | $771,125 | $958,350 | $150,000 | $323.7 |

| KENDALL | $498,257 | $637,950 | $771,125 | $958,350 | $400,000 | $323.7 |

| KNOX | $498,257 | $637,950 | $771,125 | $958,350 | $91,000 | $323.7 |

| LAKE | $498,257 | $637,950 | $771,125 | $958,350 | $400,000 | $323.7 |

| LASALLE | $498,257 | $637,950 | $771,125 | $958,350 | $320,000 | $323.7 |

| LAWRENCE | $498,257 | $637,950 | $771,125 | $958,350 | $55,000 | $323.7 |

| LEE | $498,257 | $637,950 | $771,125 | $958,350 | $120,000 | $323.7 |

| LIVINGSTON | $498,257 | $637,950 | $771,125 | $958,350 | $110,000 | $323.7 |

| LOGAN | $498,257 | $637,950 | $771,125 | $958,350 | $96,000 | $323.7 |

| MCDONOUGH | $498,257 | $637,950 | $771,125 | $958,350 | $74,000 | $323.7 |

| MCHENRY | $498,257 | $637,950 | $771,125 | $958,350 | $400,000 | $323.7 |

| MCLEAN | $498,257 | $637,950 | $771,125 | $958,350 | $200,000 | $323.7 |

| MACON | $498,257 | $637,950 | $771,125 | $958,350 | $109,000 | $323.7 |

| MACOUPIN | $498,257 | $637,950 | $771,125 | $958,350 | $350,000 | $323.7 |

| MADISON | $498,257 | $637,950 | $771,125 | $958,350 | $350,000 | $323.7 |

| MARION | $498,257 | $637,950 | $771,125 | $958,350 | $72,000 | $323.7 |

| MARSHALL | $498,257 | $637,950 | $771,125 | $958,350 | $150,000 | $323.7 |

| MASON | $498,257 | $637,950 | $771,125 | $958,350 | $72,000 | $323.7 |

| MASSAC | $498,257 | $637,950 | $771,125 | $958,350 | $153,000 | $323.7 |

| MENARD | $498,257 | $637,950 | $771,125 | $958,350 | $140,000 | $323.7 |

| MERCER | $498,257 | $637,950 | $771,125 | $958,350 | $195,000 | $323.7 |

| MONROE | $498,257 | $637,950 | $771,125 | $958,350 | $350,000 | $323.7 |

| MONTGOMERY | $498,257 | $637,950 | $771,125 | $958,350 | $80,000 | $323.7 |

| MORGAN | $498,257 | $637,950 | $771,125 | $958,350 | $105,000 | $323.7 |

| MOULTRIE | $498,257 | $637,950 | $771,125 | $958,350 | $97,000 | $323.7 |

| OGLE | $498,257 | $637,950 | $771,125 | $958,350 | $152,000 | $323.7 |

| PEORIA | $498,257 | $637,950 | $771,125 | $958,350 | $150,000 | $323.7 |

| PERRY | $498,257 | $637,950 | $771,125 | $958,350 | $78,000 | $323.7 |

| PIATT | $498,257 | $637,950 | $771,125 | $958,350 | $190,000 | $323.7 |

| PIKE | $498,257 | $637,950 | $771,125 | $958,350 | $94,000 | $323.7 |

| POPE | $498,257 | $637,950 | $771,125 | $958,350 | $44,000 | $323.7 |

| PULASKI | $498,257 | $637,950 | $771,125 | $958,350 | $84,000 | $323.7 |

| PUTNAM | $498,257 | $637,950 | $771,125 | $958,350 | $320,000 | $323.7 |

| RANDOLPH | $498,257 | $637,950 | $771,125 | $958,350 | $93,000 | $323.7 |

| RICHLAND | $498,257 | $637,950 | $771,125 | $958,350 | $115,000 | $323.7 |

| ROCK ISLAND | $498,257 | $637,950 | $771,125 | $958,350 | $195,000 | $323.7 |

| ST. CLAIR | $498,257 | $637,950 | $771,125 | $958,350 | $350,000 | $323.7 |

| SALINE | $498,257 | $637,950 | $771,125 | $958,350 | $58,000 | $323.7 |

| SANGAMON | $498,257 | $637,950 | $771,125 | $958,350 | $140,000 | $323.7 |

| SCHUYLER | $498,257 | $637,950 | $771,125 | $958,350 | $82,000 | $323.7 |

| SCOTT | $498,257 | $637,950 | $771,125 | $958,350 | $105,000 | $323.7 |

| SHELBY | $498,257 | $637,950 | $771,125 | $958,350 | $95,000 | $323.7 |

| STARK | $498,257 | $637,950 | $771,125 | $958,350 | $150,000 | $323.7 |

| STEPHENSON | $498,257 | $637,950 | $771,125 | $958,350 | $133,000 | $323.7 |

| TAZEWELL | $498,257 | $637,950 | $771,125 | $958,350 | $150,000 | $323.7 |

| UNION | $498,257 | $637,950 | $771,125 | $958,350 | $140,000 | $323.7 |

| VERMILION | $498,257 | $637,950 | $771,125 | $958,350 | $75,000 | $323.7 |

| WABASH | $498,257 | $637,950 | $771,125 | $958,350 | $102,000 | $323.7 |

| WARREN | $498,257 | $637,950 | $771,125 | $958,350 | $87,000 | $323.7 |

| WASHINGTON | $498,257 | $637,950 | $771,125 | $958,350 | $120,000 | $323.7 |

| WAYNE | $498,257 | $637,950 | $771,125 | $958,350 | $66,000 | $323.7 |

| WHITE | $498,257 | $637,950 | $771,125 | $958,350 | $74,000 | $323.7 |

| WHITESIDE | $498,257 | $637,950 | $771,125 | $958,350 | $100,000 | $323.7 |

| WILL | $498,257 | $637,950 | $771,125 | $958,350 | $400,000 | $323.7 |

| WILLIAMSON | $498,257 | $637,950 | $771,125 | $958,350 | $146,000 | $323.7 |

| WINNEBAGO | $498,257 | $637,950 | $771,125 | $958,350 | $206,000 | $323.7 |

| WOODFORD | $498,257 | $637,950 | $771,125 | $958,350 | $150,000 | $323.7 |

| ADAMS | $498,257 | $637,950 | $771,125 | $958,350 | $163,000 | $323.7 |

| ALLEN | $498,257 | $637,950 | $771,125 | $958,350 | $243,000 | $323.7 |

| BARTHOLOMEW | $498,257 | $637,950 | $771,125 | $958,350 | $250,000 | $323.7 |

| BENTON | $498,257 | $637,950 | $771,125 | $958,350 | $249,000 | $323.7 |

| BLACKFORD | $498,257 | $637,950 | $771,125 | $958,350 | $111,000 | $323.7 |

| BOONE | $498,257 | $637,950 | $771,125 | $958,350 | $425,000 | $323.7 |

| BROWN | $498,257 | $637,950 | $771,125 | $958,350 | $425,000 | $323.7 |

| CARROLL | $498,257 | $637,950 | $771,125 | $958,350 | $249,000 | $323.7 |

| CASS | $498,257 | $637,950 | $771,125 | $958,350 | $142,000 | $323.7 |

| CLARK | $498,257 | $637,950 | $771,125 | $958,350 | $390,000 | $323.7 |

| CLAY | $498,257 | $637,950 | $771,125 | $958,350 | $134,000 | $323.7 |

| CLINTON | $498,257 | $637,950 | $771,125 | $958,350 | $180,000 | $323.7 |

| CRAWFORD | $498,257 | $637,950 | $771,125 | $958,350 | $111,000 | $323.7 |

| DAVIESS | $498,257 | $637,950 | $771,125 | $958,350 | $120,000 | $323.7 |

| DEARBORN | $498,257 | $637,950 | $771,125 | $958,350 | $335,000 | $323.7 |

| DECATUR | $498,257 | $637,950 | $771,125 | $958,350 | $195,000 | $323.7 |

| DEKALB | $498,257 | $637,950 | $771,125 | $958,350 | $199,000 | $323.7 |

| DELAWARE | $498,257 | $637,950 | $771,125 | $958,350 | $158,000 | $323.7 |

| DUBOIS | $498,257 | $637,950 | $771,125 | $958,350 | $200,000 | $323.7 |

| ELKHART | $498,257 | $637,950 | $771,125 | $958,350 | $230,000 | $323.7 |

| FAYETTE | $498,257 | $637,950 | $771,125 | $958,350 | $100,000 | $323.7 |

| FLOYD | $498,257 | $637,950 | $771,125 | $958,350 | $390,000 | $323.7 |

| FOUNTAIN | $498,257 | $637,950 | $771,125 | $958,350 | $158,000 | $323.7 |

| FRANKLIN | $498,257 | $637,950 | $771,125 | $958,350 | $335,000 | $323.7 |

| FULTON | $498,257 | $637,950 | $771,125 | $958,350 | $170,000 | $323.7 |

| GIBSON | $498,257 | $637,950 | $771,125 | $958,350 | $139,000 | $323.7 |

| GRANT | $498,257 | $637,950 | $771,125 | $958,350 | $125,000 | $323.7 |

| GREENE | $498,257 | $637,950 | $771,125 | $958,350 | $153,000 | $323.7 |

| HAMILTON | $498,257 | $637,950 | $771,125 | $958,350 | $425,000 | $323.7 |

| HANCOCK | $498,257 | $637,950 | $771,125 | $958,350 | $425,000 | $323.7 |

| HARRISON | $498,257 | $637,950 | $771,125 | $958,350 | $390,000 | $323.7 |

| HENDRICKS | $498,257 | $637,950 | $771,125 | $958,350 | $425,000 | $323.7 |

| HENRY | $498,257 | $637,950 | $771,125 | $958,350 | $150,000 | $323.7 |

| HOWARD | $498,257 | $637,950 | $771,125 | $958,350 | $161,000 | $323.7 |

| HUNTINGTON | $498,257 | $637,950 | $771,125 | $958,350 | $155,000 | $323.7 |

| JACKSON | $498,257 | $637,950 | $771,125 | $958,350 | $196,000 | $323.7 |

| JASPER | $498,257 | $637,950 | $771,125 | $958,350 | $400,000 | $323.7 |

| JAY | $498,257 | $637,950 | $771,125 | $958,350 | $124,000 | $323.7 |

| JEFFERSON | $498,257 | $637,950 | $771,125 | $958,350 | $171,000 | $323.7 |

| JENNINGS | $498,257 | $637,950 | $771,125 | $958,350 | $184,000 | $323.7 |

| JOHNSON | $498,257 | $637,950 | $771,125 | $958,350 | $425,000 | $323.7 |

| KNOX | $498,257 | $637,950 | $771,125 | $958,350 | $137,000 | $323.7 |

| KOSCIUSKO | $498,257 | $637,950 | $771,125 | $958,350 | $238,000 | $323.7 |

| LAGRANGE | $498,257 | $637,950 | $771,125 | $958,350 | $235,000 | $323.7 |

| LAKE | $498,257 | $637,950 | $771,125 | $958,350 | $400,000 | $323.7 |

| LAPORTE | $498,257 | $637,950 | $771,125 | $958,350 | $198,000 | $323.7 |

| LAWRENCE | $498,257 | $637,950 | $771,125 | $958,350 | $120,000 | $323.7 |

| MADISON | $498,257 | $637,950 | $771,125 | $958,350 | $425,000 | $323.7 |

| MARION | $498,257 | $637,950 | $771,125 | $958,350 | $425,000 | $323.7 |

| MARSHALL | $498,257 | $637,950 | $771,125 | $958,350 | $206,000 | $323.7 |

| MARTIN | $498,257 | $637,950 | $771,125 | $958,350 | $109,000 | $323.7 |

| MIAMI | $498,257 | $637,950 | $771,125 | $958,350 | $126,000 | $323.7 |

| MONROE | $498,257 | $637,950 | $771,125 | $958,350 | $305,000 | $323.7 |

| MONTGOMERY | $498,257 | $637,950 | $771,125 | $958,350 | $181,000 | $323.7 |

| MORGAN | $498,257 | $637,950 | $771,125 | $958,350 | $425,000 | $323.7 |

| NEWTON | $498,257 | $637,950 | $771,125 | $958,350 | $400,000 | $323.7 |

| NOBLE | $498,257 | $637,950 | $771,125 | $958,350 | $188,000 | $323.7 |

| OHIO | $498,257 | $637,950 | $771,125 | $958,350 | $335,000 | $323.7 |

| ORANGE | $498,257 | $637,950 | $771,125 | $958,350 | $130,000 | $323.7 |

| OWEN | $498,257 | $637,950 | $771,125 | $958,350 | $305,000 | $323.7 |

| PARKE | $498,257 | $637,950 | $771,125 | $958,350 | $134,000 | $323.7 |

| PERRY | $498,257 | $637,950 | $771,125 | $958,350 | $149,000 | $323.7 |

| PIKE | $498,257 | $637,950 | $771,125 | $958,350 | $200,000 | $323.7 |

| PORTER | $498,257 | $637,950 | $771,125 | $958,350 | $400,000 | $323.7 |

| POSEY | $498,257 | $637,950 | $771,125 | $958,350 | $254,000 | $323.7 |

| PULASKI | $498,257 | $637,950 | $771,125 | $958,350 | $155,000 | $323.7 |

| PUTNAM | $498,257 | $637,950 | $771,125 | $958,350 | $425,000 | $323.7 |

| RANDOLPH | $498,257 | $637,950 | $771,125 | $958,350 | $114,000 | $323.7 |

| RIPLEY | $498,257 | $637,950 | $771,125 | $958,350 | $194,000 | $323.7 |

| RUSH | $498,257 | $637,950 | $771,125 | $958,350 | $162,000 | $323.7 |

| ST. JOSEPH | $498,257 | $637,950 | $771,125 | $958,350 | $189,000 | $323.7 |

| SCOTT | $498,257 | $637,950 | $771,125 | $958,350 | $171,000 | $323.7 |

| SHELBY | $498,257 | $637,950 | $771,125 | $958,350 | $425,000 | $323.7 |

| SPENCER | $498,257 | $637,950 | $771,125 | $958,350 | $168,000 | $323.7 |

| STARKE | $498,257 | $637,950 | $771,125 | $958,350 | $184,000 | $323.7 |

| STEUBEN | $498,257 | $637,950 | $771,125 | $958,350 | $214,000 | $323.7 |

| SULLIVAN | $498,257 | $637,950 | $771,125 | $958,350 | $134,000 | $323.7 |

| SWITZERLAND | $498,257 | $637,950 | $771,125 | $958,350 | $105,000 | $323.7 |

| TIPPECANOE | $498,257 | $637,950 | $771,125 | $958,350 | $249,000 | $323.7 |

| TIPTON | $498,257 | $637,950 | $771,125 | $958,350 | $140,000 | $323.7 |

| UNION | $498,257 | $637,950 | $771,125 | $958,350 | $335,000 | $323.7 |

| VANDERBURGH | $498,257 | $637,950 | $771,125 | $958,350 | $254,000 | $323.7 |

| VERMILLION | $498,257 | $637,950 | $771,125 | $958,350 | $134,000 | $323.7 |

| VIGO | $498,257 | $637,950 | $771,125 | $958,350 | $134,000 | $323.7 |

| WABASH | $498,257 | $637,950 | $771,125 | $958,350 | $164,000 | $323.7 |

| WARREN | $498,257 | $637,950 | $771,125 | $958,350 | $249,000 | $323.7 |

| WARRICK | $498,257 | $637,950 | $771,125 | $958,350 | $254,000 | $323.7 |

| WASHINGTON | $498,257 | $637,950 | $771,125 | $958,350 | $390,000 | $323.7 |

| WAYNE | $498,257 | $637,950 | $771,125 | $958,350 | $141,000 | $323.7 |

| WELLS | $498,257 | $637,950 | $771,125 | $958,350 | $188,000 | $323.7 |

| WHITE | $498,257 | $637,950 | $771,125 | $958,350 | $177,000 | $323.7 |

| WHITLEY | $498,257 | $637,950 | $771,125 | $958,350 | $243,000 | $323.7 |

| DICKINSON | $498,257 | $637,950 | $771,125 | $958,350 | $158,000 | $323.7 |

| FINNEY | $498,257 | $637,950 | $771,125 | $958,350 | $258,000 | $323.7 |

| FRANKLIN | $498,257 | $637,950 | $771,125 | $958,350 | $199,000 | $323.7 |

| KINGMAN | $498,257 | $637,950 | $771,125 | $958,350 | $126,000 | $323.7 |

| LINCOLN | $498,257 | $637,950 | $771,125 | $958,350 | $110,000 | $323.7 |

| LINN | $498,257 | $637,950 | $771,125 | $958,350 | $427,000 | $323.7 |

| RAWLINS | $498,257 | $637,950 | $771,125 | $958,350 | $131,000 | $323.7 |

| SALINE | $498,257 | $637,950 | $771,125 | $958,350 | $187,000 | $323.7 |

| WASHINGTON | $498,257 | $637,950 | $771,125 | $958,350 | $117,000 | $323.7 |

| BRECKINRIDGE | $498,257 | $637,950 | $771,125 | $958,350 | $83,000 | $323.7 |

| CLINTON | $498,257 | $637,950 | $771,125 | $958,350 | $40,000 | $323.7 |

| FLEMING | $498,257 | $637,950 | $771,125 | $958,350 | $80,000 | $323.7 |

| FRANKLIN | $498,257 | $637,950 | $771,125 | $958,350 | $243,000 | $323.7 |

| GALLATIN | $498,257 | $637,950 | $771,125 | $958,350 | $335,000 | $323.7 |

| HARDIN | $498,257 | $637,950 | $771,125 | $958,350 | $201,000 | $323.7 |

| HOPKINS | $498,257 | $637,950 | $771,125 | $958,350 | $118,000 | $323.7 |

| JESSAMINE | $498,257 | $637,950 | $771,125 | $958,350 | $277,000 | $323.7 |

| LINCOLN | $498,257 | $637,950 | $771,125 | $958,350 | $180,000 | $323.7 |

| LIVINGSTON | $498,257 | $637,950 | $771,125 | $958,350 | $153,000 | $323.7 |

| MAGOFFIN | $498,257 | $637,950 | $771,125 | $958,350 | $17,000 | $323.7 |

| MARTIN | $498,257 | $637,950 | $771,125 | $958,350 | $113,000 | $323.7 |

| WASHINGTON | $498,257 | $637,950 | $771,125 | $958,350 | $155,000 | $323.7 |

| EVANGELINE | $498,257 | $637,950 | $771,125 | $958,350 | $48,000 | $323.7 |

| FRANKLIN | $498,257 | $637,950 | $771,125 | $958,350 | $30,000 | $323.7 |

| LINCOLN | $498,257 | $637,950 | $771,125 | $958,350 | $211,000 | $323.7 |

| LIVINGSTON | $498,257 | $637,950 | $771,125 | $958,350 | $263,000 | $323.7 |

| PLAQUEMINES | $498,257 | $637,950 | $771,125 | $958,350 | $300,000 | $323.7 |

| POINTE COUPEE | $498,257 | $637,950 | $771,125 | $958,350 | $263,000 | $323.7 |

| SABINE | $498,257 | $637,950 | $771,125 | $958,350 | $115,000 | $323.7 |

| ST. MARTIN | $498,257 | $637,950 | $771,125 | $958,350 | $217,000 | $323.7 |

| WASHINGTON | $498,257 | $637,950 | $771,125 | $958,350 | $66,000 | $323.7 |

| WINN | $498,257 | $637,950 | $771,125 | $958,350 | $112,000 | $323.7 |

| FRANKLIN | $498,257 | $637,950 | $771,125 | $958,350 | $375,000 | $323.7 |

| CAROLINE | $498,257 | $637,950 | $771,125 | $958,350 | $225,000 | $323.7 |

| PRINCE GEORGE’S | $1,149,825 | $1,472,250 | $1,779,525 | $2,211,600 | $72,000 | $0.65 |

| WASHINGTON | $498,257 | $637,950 | $771,125 | $958,350 | $269,000 | $323.7 |

| ANDROSCOGGIN | $498,257 | $637,950 | $771,125 | $958,350 | $280,000 | $323.7 |

| AROOSTOOK | $498,257 | $637,950 | $771,125 | $958,350 | $140,000 | $323.7 |

| CUMBERLAND | $546,250 | $699,300 | $845,300 | $1,050,500 | $475,000 | $354.9 |

| FRANKLIN | $498,257 | $637,950 | $771,125 | $958,350 | $210,000 | $323.7 |

| HANCOCK | $498,257 | $637,950 | $771,125 | $958,350 | $290,000 | $323.7 |

| KENNEBEC | $498,257 | $637,950 | $771,125 | $958,350 | $255,000 | $323.7 |

| KNOX | $498,257 | $637,950 | $771,125 | $958,350 | $326,000 | $323.7 |

| LINCOLN | $498,257 | $637,950 | $771,125 | $958,350 | $290,000 | $323.7 |

| OXFORD | $498,257 | $637,950 | $771,125 | $958,350 | $265,000 | $323.7 |

| PENOBSCOT | $498,257 | $637,950 | $771,125 | $958,350 | $228,000 | $323.7 |

| PISCATAQUIS | $498,257 | $637,950 | $771,125 | $958,350 | $190,000 | $323.7 |

| SAGADAHOC | $546,250 | $699,300 | $845,300 | $1,050,500 | $475,000 | $354.9 |

| SOMERSET | $498,257 | $637,950 | $771,125 | $958,350 | $195,000 | $323.7 |

| WALDO | $498,257 | $637,950 | $771,125 | $958,350 | $262,000 | $323.7 |

| WASHINGTON | $498,257 | $637,950 | $771,125 | $958,350 | $170,000 | $323.7 |

| YORK | $546,250 | $699,300 | $845,300 | $1,050,500 | $475,000 | $354.9 |

| CLINTON | $498,257 | $637,950 | $771,125 | $958,350 | $226,000 | $323.7 |

| DICKINSON | $498,257 | $637,950 | $771,125 | $958,350 | $110,000 | $323.7 |

| GLADWIN | $498,257 | $637,950 | $771,125 | $958,350 | $124,000 | $323.7 |

| INGHAM | $498,257 | $637,950 | $771,125 | $958,350 | $226,000 | $323.7 |

| LIVINGSTON | $498,257 | $637,950 | $771,125 | $958,350 | $325,000 | $323.7 |

| MACKINAC | $498,257 | $637,950 | $771,125 | $958,350 | $224,000 | $323.7 |

| MENOMINEE | $498,257 | $637,950 | $771,125 | $958,350 | $115,000 | $323.7 |

| SAGINAW | $498,257 | $637,950 | $771,125 | $958,350 | $126,000 | $323.7 |

| AITKIN | $498,257 | $637,950 | $771,125 | $958,350 | $186,000 | $323.7 |

| ANOKA | $515,200 | $659,550 | $797,250 | $990,800 | $442,000 | $334.75 |

| BECKER | $498,257 | $637,950 | $771,125 | $958,350 | $227,000 | $323.7 |

| BELTRAMI | $498,257 | $637,950 | $771,125 | $958,350 | $192,000 | $323.7 |

| BENTON | $498,257 | $637,950 | $771,125 | $958,350 | $249,000 | $323.7 |

| BIG STONE | $498,257 | $637,950 | $771,125 | $958,350 | $128,000 | $323.7 |

| BLUE EARTH | $498,257 | $637,950 | $771,125 | $958,350 | $260,000 | $323.7 |

| BROWN | $498,257 | $637,950 | $771,125 | $958,350 | $169,000 | $323.7 |

| CARLTON | $498,257 | $637,950 | $771,125 | $958,350 | $200,000 | $323.7 |

| CARVER | $515,200 | $659,550 | $797,250 | $990,800 | $442,000 | $334.75 |

| CASS | $498,257 | $637,950 | $771,125 | $958,350 | $245,000 | $323.7 |

| CHIPPEWA | $498,257 | $637,950 | $771,125 | $958,350 | $111,000 | $323.7 |

| CHISAGO | $515,200 | $659,550 | $797,250 | $990,800 | $442,000 | $334.75 |

| CLAY | $498,257 | $637,950 | $771,125 | $958,350 | $290,000 | $323.7 |

| CLEARWATER | $498,257 | $637,950 | $771,125 | $958,350 | $122,000 | $323.7 |

| COOK | $498,257 | $637,950 | $771,125 | $958,350 | $220,000 | $323.7 |

| COTTONWOOD | $498,257 | $637,950 | $771,125 | $958,350 | $130,000 | $323.7 |

| CROW WING | $498,257 | $637,950 | $771,125 | $958,350 | $245,000 | $323.7 |

| DAKOTA | $515,200 | $659,550 | $797,250 | $990,800 | $442,000 | $334.75 |

| DODGE | $498,257 | $637,950 | $771,125 | $958,350 | $300,000 | $323.7 |

| DOUGLAS | $498,257 | $637,950 | $771,125 | $958,350 | $250,000 | $323.7 |

| FARIBAULT | $498,257 | $637,950 | $771,125 | $958,350 | $94,000 | $323.7 |

| FILLMORE | $498,257 | $637,950 | $771,125 | $958,350 | $300,000 | $323.7 |

| FREEBORN | $498,257 | $637,950 | $771,125 | $958,350 | $140,000 | $323.7 |

| GOODHUE | $498,257 | $637,950 | $771,125 | $958,350 | $258,000 | $323.7 |

| GRANT | $498,257 | $637,950 | $771,125 | $958,350 | $125,000 | $323.7 |

| HENNEPIN | $515,200 | $659,550 | $797,250 | $990,800 | $442,000 | $334.75 |

| HOUSTON | $498,257 | $637,950 | $771,125 | $958,350 | $244,000 | $323.7 |

| HUBBARD | $498,257 | $637,950 | $771,125 | $958,350 | $175,000 | $323.7 |

| ISANTI | $515,200 | $659,550 | $797,250 | $990,800 | $442,000 | $334.75 |

| ITASCA | $498,257 | $637,950 | $771,125 | $958,350 | $169,000 | $323.7 |

| JACKSON | $498,257 | $637,950 | $771,125 | $958,350 | $125,000 | $323.7 |

| KANABEC | $498,257 | $637,950 | $771,125 | $958,350 | $200,000 | $323.7 |

| KANDIYOHI | $498,257 | $637,950 | $771,125 | $958,350 | $200,000 | $323.7 |

| KITTSON | $498,257 | $637,950 | $771,125 | $958,350 | $97,000 | $323.7 |

| KOOCHICHING | $498,257 | $637,950 | $771,125 | $958,350 | $99,000 | $323.7 |

| LAC QUI PARLE | $498,257 | $637,950 | $771,125 | $958,350 | $98,000 | $323.7 |

| LAKE | $498,257 | $637,950 | $771,125 | $958,350 | $200,000 | $323.7 |

| LAKE OF THE WOO | $498,257 | $637,950 | $771,125 | $958,350 | $100,000 | $323.7 |

| LE SUEUR | $515,200 | $659,550 | $797,250 | $990,800 | $442,000 | $334.75 |

| LINCOLN | $498,257 | $637,950 | $771,125 | $958,350 | $79,000 | $323.7 |

| LYON | $498,257 | $637,950 | $771,125 | $958,350 | $145,000 | $323.7 |

| MCLEOD | $498,257 | $637,950 | $771,125 | $958,350 | $235,000 | $323.7 |

| MAHNOMEN | $498,257 | $637,950 | $771,125 | $958,350 | $100,000 | $323.7 |

| MARSHALL | $498,257 | $637,950 | $771,125 | $958,350 | $122,000 | $323.7 |

| MARTIN | $498,257 | $637,950 | $771,125 | $958,350 | $116,000 | $323.7 |

| MEEKER | $498,257 | $637,950 | $771,125 | $958,350 | $192,000 | $323.7 |

| MILLE LACS | $515,200 | $659,550 | $797,250 | $990,800 | $442,000 | $334.75 |

| MORRISON | $498,257 | $637,950 | $771,125 | $958,350 | $194,000 | $323.7 |

| MOWER | $498,257 | $637,950 | $771,125 | $958,350 | $150,000 | $323.7 |

| MURRAY | $498,257 | $637,950 | $771,125 | $958,350 | $102,000 | $323.7 |

| NICOLLET | $498,257 | $637,950 | $771,125 | $958,350 | $260,000 | $323.7 |

| NOBLES | $498,257 | $637,950 | $771,125 | $958,350 | $180,000 | $323.7 |

| NORMAN | $498,257 | $637,950 | $771,125 | $958,350 | $98,000 | $323.7 |

| OLMSTED | $498,257 | $637,950 | $771,125 | $958,350 | $300,000 | $323.7 |

| OTTER TAIL | $498,257 | $637,950 | $771,125 | $958,350 | $217,000 | $323.7 |

| PENNINGTON | $498,257 | $637,950 | $771,125 | $958,350 | $174,000 | $323.7 |

| PINE | $498,257 | $637,950 | $771,125 | $958,350 | $210,000 | $323.7 |

| PIPESTONE | $498,257 | $637,950 | $771,125 | $958,350 | $97,000 | $323.7 |

| POLK | $498,257 | $637,950 | $771,125 | $958,350 | $245,000 | $323.7 |

| POPE | $498,257 | $637,950 | $771,125 | $958,350 | $196,000 | $323.7 |

| RAMSEY | $515,200 | $659,550 | $797,250 | $990,800 | $442,000 | $334.75 |

| RED LAKE | $498,257 | $637,950 | $771,125 | $958,350 | $112,000 | $323.7 |

| REDWOOD | $498,257 | $637,950 | $771,125 | $958,350 | $100,000 | $323.7 |

| RENVILLE | $498,257 | $637,950 | $771,125 | $958,350 | $130,000 | $323.7 |

| RICE | $498,257 | $637,950 | $771,125 | $958,350 | $285,000 | $323.7 |

| ROCK | $498,257 | $637,950 | $771,125 | $958,350 | $175,000 | $323.7 |

| ROSEAU | $498,257 | $637,950 | $771,125 | $958,350 | $169,000 | $323.7 |

| ST. LOUIS | $498,257 | $637,950 | $771,125 | $958,350 | $200,000 | $323.7 |

| SCOTT | $515,200 | $659,550 | $797,250 | $990,800 | $442,000 | $334.75 |

| SHERBURNE | $515,200 | $659,550 | $797,250 | $990,800 | $442,000 | $334.75 |

| SIBLEY | $498,257 | $637,950 | $771,125 | $958,350 | $200,000 | $323.7 |

| STEARNS | $498,257 | $637,950 | $771,125 | $958,350 | $249,000 | $323.7 |

| STEELE | $498,257 | $637,950 | $771,125 | $958,350 | $235,000 | $323.7 |

| STEVENS | $498,257 | $637,950 | $771,125 | $958,350 | $139,000 | $323.7 |

| SWIFT | $498,257 | $637,950 | $771,125 | $958,350 | $86,000 | $323.7 |

| TODD | $498,257 | $637,950 | $771,125 | $958,350 | $144,000 | $323.7 |

| TRAVERSE | $498,257 | $637,950 | $771,125 | $958,350 | $55,000 | $323.7 |

| WABASHA | $498,257 | $637,950 | $771,125 | $958,350 | $300,000 | $323.7 |

| WADENA | $498,257 | $637,950 | $771,125 | $958,350 | $160,000 | $323.7 |

| WASECA | $498,257 | $637,950 | $771,125 | $958,350 | $200,000 | $323.7 |

| WASHINGTON | $515,200 | $659,550 | $797,250 | $990,800 | $442,000 | $334.75 |

| WATONWAN | $498,257 | $637,950 | $771,125 | $958,350 | $131,000 | $323.7 |

| WILKIN | $498,257 | $637,950 | $771,125 | $958,350 | $185,000 | $323.7 |

| WINONA | $498,257 | $637,950 | $771,125 | $958,350 | $210,000 | $323.7 |

| WRIGHT | $515,200 | $659,550 | $797,250 | $990,800 | $442,000 | $334.75 |

| YELLOW MEDICINE | $498,257 | $637,950 | $771,125 | $958,350 | $96,000 | $323.7 |

| AUDRAIN | $498,257 | $637,950 | $771,125 | $958,350 | $136,000 | $323.7 |

| BOLLINGER | $498,257 | $637,950 | $771,125 | $958,350 | $205,000 | $323.7 |

| CLINTON | $498,257 | $637,950 | $771,125 | $958,350 | $427,000 | $323.7 |

| DUNKLIN | $498,257 | $637,950 | $771,125 | $958,350 | $120,000 | $323.7 |

| FRANKLIN | $498,257 | $637,950 | $771,125 | $958,350 | $350,000 | $323.7 |

| LINCOLN | $498,257 | $637,950 | $771,125 | $958,350 | $350,000 | $323.7 |

| LINN | $498,257 | $637,950 | $771,125 | $958,350 | $109,000 | $323.7 |

| LIVINGSTON | $498,257 | $637,950 | $771,125 | $958,350 | $144,000 | $323.7 |

| SALINE | $498,257 | $637,950 | $771,125 | $958,350 | $143,000 | $323.7 |

| WASHINGTON | $498,257 | $637,950 | $771,125 | $958,350 | $151,000 | $323.7 |

| WASHINGTON | $498,257 | $637,950 | $771,125 | $958,350 | $151,000 | $323.7 |

| COVINGTON | $498,257 | $637,950 | $771,125 | $958,350 | $258,000 | $323.7 |

| FRANKLIN | $498,257 | $637,950 | $771,125 | $958,350 | $112,000 | $323.7 |

| HINDS | $498,257 | $637,950 | $771,125 | $958,350 | $322,000 | $323.7 |

| LINCOLN | $498,257 | $637,950 | $771,125 | $958,350 | $177,000 | $323.7 |

| RANKIN | $498,257 | $637,950 | $771,125 | $958,350 | $322,000 | $323.7 |

| TISHOMINGO | $498,257 | $637,950 | $771,125 | $958,350 | $139,000 | $323.7 |

| WASHINGTON | $498,257 | $637,950 | $771,125 | $958,350 | $106,000 | $323.7 |

| WILKINSON | $498,257 | $637,950 | $771,125 | $958,350 | $91,000 | $323.7 |

| WINSTON | $498,257 | $637,950 | $771,125 | $958,350 | $134,000 | $323.7 |

| BLAINE | $498,257 | $637,950 | $771,125 | $958,350 | $297,000 | $323.7 |

| GALLATIN | $718,750 | $920,150 | $1,112,250 | $1,382,250 | $625,000 | $466.7 |

| JUDITH BASIN | $498,257 | $637,950 | $771,125 | $958,350 | $207,000 | $323.7 |

| LINCOLN | $498,257 | $637,950 | $771,125 | $958,350 | $307,000 | $323.7 |

| MINERAL | $498,257 | $637,950 | $771,125 | $958,350 | $322,000 | $323.7 |

| ALAMANCE | $498,257 | $637,950 | $771,125 | $958,350 | $265,000 | $323.7 |

| ALEXANDER | $498,257 | $637,950 | $771,125 | $958,350 | $226,000 | $323.7 |

| ALLEGHANY | $498,257 | $637,950 | $771,125 | $958,350 | $113,000 | $323.7 |

| ANSON | $498,257 | $637,950 | $771,125 | $958,350 | $420,000 | $323.7 |

| ASHE | $498,257 | $637,950 | $771,125 | $958,350 | $100,000 | $323.7 |

| AVERY | $498,257 | $637,950 | $771,125 | $958,350 | $214,000 | $323.7 |

| BEAUFORT | $498,257 | $637,950 | $771,125 | $958,350 | $181,000 | $323.7 |

| BERTIE | $498,257 | $637,950 | $771,125 | $958,350 | $56,000 | $323.7 |

| BLADEN | $498,257 | $637,950 | $771,125 | $958,350 | $115,000 | $323.7 |

| BRUNSWICK | $498,257 | $637,950 | $771,125 | $958,350 | $335,000 | $323.7 |

| BUNCOMBE | $498,257 | $637,950 | $771,125 | $958,350 | $408,000 | $323.7 |

| BURKE | $498,257 | $637,950 | $771,125 | $958,350 | $226,000 | $323.7 |

| CABARRUS | $498,257 | $637,950 | $771,125 | $958,350 | $420,000 | $323.7 |

| CALDWELL | $498,257 | $637,950 | $771,125 | $958,350 | $226,000 | $323.7 |

| CAMDEN | $690,000 | $883,300 | $1,067,750 | $1,326,950 | $600,000 | $448.5 |

| CARTERET | $498,257 | $637,950 | $771,125 | $958,350 | $335,000 | $323.7 |

| CASWELL | $498,257 | $637,950 | $771,125 | $958,350 | $120,000 | $323.7 |

| CATAWBA | $498,257 | $637,950 | $771,125 | $958,350 | $226,000 | $323.7 |

| CHATHAM | $602,600 | $771,450 | $932,500 | $1,158,850 | $513,000 | $391.3 |

| CHEROKEE | $498,257 | $637,950 | $771,125 | $958,350 | $184,000 | $323.7 |

| CHOWAN | $498,257 | $637,950 | $771,125 | $958,350 | $192,000 | $323.7 |

| CLAY | $498,257 | $637,950 | $771,125 | $958,350 | $180,000 | $323.7 |

| CLEVELAND | $498,257 | $637,950 | $771,125 | $958,350 | $170,000 | $323.7 |

| COLUMBUS | $498,257 | $637,950 | $771,125 | $958,350 | $99,000 | $323.7 |

| CRAVEN | $498,257 | $637,950 | $771,125 | $958,350 | $256,000 | $323.7 |

| CUMBERLAND | $498,257 | $637,950 | $771,125 | $958,350 | $300,000 | $323.7 |

| CURRITUCK | $690,000 | $883,300 | $1,067,750 | $1,326,950 | $600,000 | $448.5 |

| DARE | $617,550 | $790,550 | $955,600 | $1,187,600 | $537,000 | $401.05 |

| DAVIDSON | $498,257 | $637,950 | $771,125 | $958,350 | $255,000 | $323.7 |

| DAVIE | $498,257 | $637,950 | $771,125 | $958,350 | $255,000 | $323.7 |

| DUPLIN | $498,257 | $637,950 | $771,125 | $958,350 | $125,000 | $323.7 |

| DURHAM | $602,600 | $771,450 | $932,500 | $1,158,850 | $513,000 | $391.3 |

| EDGECOMBE | $498,257 | $637,950 | $771,125 | $958,350 | $205,000 | $323.7 |

| FORSYTH | $498,257 | $637,950 | $771,125 | $958,350 | $255,000 | $323.7 |

| FRANKLIN | $529,000 | $677,200 | $818,600 | $1,017,300 | $460,000 | $343.85 |

| GASTON | $498,257 | $637,950 | $771,125 | $958,350 | $420,000 | $323.7 |

| GATES | $690,000 | $883,300 | $1,067,750 | $1,326,950 | $600,000 | $448.5 |

| GRAHAM | $498,257 | $637,950 | $771,125 | $958,350 | $180,000 | $323.7 |

| GRANVILLE | $602,600 | $771,450 | $932,500 | $1,158,850 | $513,000 | $391.3 |

| GREENE | $498,257 | $637,950 | $771,125 | $958,350 | $100,000 | $323.7 |

| GUILFORD | $498,257 | $637,950 | $771,125 | $958,350 | $255,000 | $323.7 |

| HALIFAX | $498,257 | $637,950 | $771,125 | $958,350 | $100,000 | $323.7 |

| HARNETT | $498,257 | $637,950 | $771,125 | $958,350 | $300,000 | $323.7 |

| HAYWOOD | $498,257 | $637,950 | $771,125 | $958,350 | $408,000 | $323.7 |

| HENDERSON | $498,257 | $637,950 | $771,125 | $958,350 | $408,000 | $323.7 |

| HERTFORD | $498,257 | $637,950 | $771,125 | $958,350 | $94,000 | $323.7 |

| HOKE | $498,257 | $637,950 | $771,125 | $958,350 | $300,000 | $323.7 |

| HYDE | $498,257 | $637,950 | $771,125 | $958,350 | $150,000 | $323.7 |

| IREDELL | $498,257 | $637,950 | $771,125 | $958,350 | $420,000 | $323.7 |

| JACKSON | $498,257 | $637,950 | $771,125 | $958,350 | $303,000 | $323.7 |

| JOHNSTON | $529,000 | $677,200 | $818,600 | $1,017,300 | $460,000 | $343.85 |

| JONES | $498,257 | $637,950 | $771,125 | $958,350 | $256,000 | $323.7 |

| LEE | $498,257 | $637,950 | $771,125 | $958,350 | $265,000 | $323.7 |

| LENOIR | $498,257 | $637,950 | $771,125 | $958,350 | $120,000 | $323.7 |

| LINCOLN | $498,257 | $637,950 | $771,125 | $958,350 | $420,000 | $323.7 |

| MCDOWELL | $498,257 | $637,950 | $771,125 | $958,350 | $110,000 | $323.7 |

| MACON | $498,257 | $637,950 | $771,125 | $958,350 | $240,000 | $323.7 |

| MADISON | $498,257 | $637,950 | $771,125 | $958,350 | $408,000 | $323.7 |

| MARTIN | $498,257 | $637,950 | $771,125 | $958,350 | $75,000 | $323.7 |

| MECKLENBURG | $498,257 | $637,950 | $771,125 | $958,350 | $420,000 | $323.7 |

| MITCHELL | $498,257 | $637,950 | $771,125 | $958,350 | $180,000 | $323.7 |

| MONTGOMERY | $498,257 | $637,950 | $771,125 | $958,350 | $86,000 | $323.7 |

| MOORE | $498,257 | $637,950 | $771,125 | $958,350 | $384,000 | $323.7 |

| NASH | $498,257 | $637,950 | $771,125 | $958,350 | $205,000 | $323.7 |

| NEW HANOVER | $498,257 | $637,950 | $771,125 | $958,350 | $395,000 | $323.7 |

| NORTHAMPTON | $498,257 | $637,950 | $771,125 | $958,350 | $100,000 | $323.7 |

| ONSLOW | $498,257 | $637,950 | $771,125 | $958,350 | $248,000 | $323.7 |

| ORANGE | $602,600 | $771,450 | $932,500 | $1,158,850 | $513,000 | $391.3 |

| PAMLICO | $498,257 | $637,950 | $771,125 | $958,350 | $256,000 | $323.7 |

| PASQUOTANK | $805,000 | $1,030,550 | $1,245,700 | $1,548,100 | $210,000 | $523.25 |

| PENDER | $498,257 | $637,950 | $771,125 | $958,350 | $395,000 | $323.7 |

| PERQUIMANS | $805,000 | $1,030,550 | $1,245,700 | $1,548,100 | $210,000 | $523.25 |

| PERSON | $602,600 | $771,450 | $932,500 | $1,158,850 | $513,000 | $391.3 |

| PITT | $498,257 | $637,950 | $771,125 | $958,350 | $239,000 | $323.7 |

| POLK | $498,257 | $637,950 | $771,125 | $958,350 | $350,000 | $323.7 |

| RANDOLPH | $498,257 | $637,950 | $771,125 | $958,350 | $255,000 | $323.7 |

| RICHMOND | $498,257 | $637,950 | $771,125 | $958,350 | $114,000 | $323.7 |

| ROBESON | $498,257 | $637,950 | $771,125 | $958,350 | $114,000 | $323.7 |

| ROCKINGHAM | $498,257 | $637,950 | $771,125 | $958,350 | $255,000 | $323.7 |

| ROWAN | $498,257 | $637,950 | $771,125 | $958,350 | $420,000 | $323.7 |

| RUTHERFORD | $498,257 | $637,950 | $771,125 | $958,350 | $190,000 | $323.7 |

| SAMPSON | $498,257 | $637,950 | $771,125 | $958,350 | $85,000 | $323.7 |

| SCOTLAND | $498,257 | $637,950 | $771,125 | $958,350 | $78,000 | $323.7 |

| STANLY | $498,257 | $637,950 | $771,125 | $958,350 | $260,000 | $323.7 |

| STOKES | $498,257 | $637,950 | $771,125 | $958,350 | $255,000 | $323.7 |

| SURRY | $498,257 | $637,950 | $771,125 | $958,350 | $135,000 | $323.7 |

| SWAIN | $498,257 | $637,950 | $771,125 | $958,350 | $303,000 | $323.7 |

| TRANSYLVANIA | $498,257 | $637,950 | $771,125 | $958,350 | $363,000 | $323.7 |

| TYRRELL | $498,257 | $637,950 | $771,125 | $958,350 | $77,000 | $323.7 |

| UNION | $498,257 | $637,950 | $771,125 | $958,350 | $420,000 | $323.7 |

| VANCE | $498,257 | $637,950 | $771,125 | $958,350 | $130,000 | $323.7 |

| WAKE | $529,000 | $677,200 | $818,600 | $1,017,300 | $460,000 | $343.85 |

| WARREN | $498,257 | $637,950 | $771,125 | $958,350 | $159,000 | $323.7 |

| WASHINGTON | $498,257 | $637,950 | $771,125 | $958,350 | $85,000 | $323.7 |

| WATAUGA | $498,257 | $637,950 | $771,125 | $958,350 | $357,000 | $323.7 |

| WAYNE | $498,257 | $637,950 | $771,125 | $958,350 | $175,000 | $323.7 |

| WILKES | $498,257 | $637,950 | $771,125 | $958,350 | $162,000 | $323.7 |

| WILSON | $498,257 | $637,950 | $771,125 | $958,350 | $167,000 | $323.7 |

| YADKIN | $498,257 | $637,950 | $771,125 | $958,350 | $255,000 | $323.7 |

| YANCEY | $498,257 | $637,950 | $771,125 | $958,350 | $225,000 | $323.7 |

| BILLINGS | $508,300 | $650,700 | $786,550 | $977,500 | $442,000 | $330.2 |

| BOTTINEAU | $498,257 | $637,950 | $771,125 | $958,350 | $130,000 | $323.7 |

| HETTINGER | $498,257 | $637,950 | $771,125 | $958,350 | $100,000 | $323.7 |

| MCINTOSH | $498,257 | $637,950 | $771,125 | $958,350 | $215,000 | $323.7 |

| PEMBINA | $498,257 | $637,950 | $771,125 | $958,350 | $87,000 | $323.7 |

| BLAINE | $498,257 | $637,950 | $771,125 | $958,350 | $116,000 | $323.7 |

| CUMING | $498,257 | $637,950 | $771,125 | $958,350 | $140,000 | $323.7 |

| FRANKLIN | $498,257 | $637,950 | $771,125 | $958,350 | $60,000 | $323.7 |

| LINCOLN | $498,257 | $637,950 | $771,125 | $958,350 | $156,000 | $323.7 |

| PERKINS | $498,257 | $637,950 | $771,125 | $958,350 | $133,000 | $323.7 |

| SALINE | $498,257 | $637,950 | $771,125 | $958,350 | $170,000 | $323.7 |

| WASHINGTON | $498,257 | $637,950 | $771,125 | $958,350 | $325,000 | $323.7 |

| ROCKINGHAM | $862,500 | $1,104,150 | $1,334,700 | $1,658,700 | $750,000 | $560.3 |

| BURLINGTON | $557,750 | $714,000 | $863,100 | $1,072,600 | $485,000 | $362.05 |

| HARDING | $498,257 | $637,950 | $771,125 | $958,350 | $188,000 | $323.7 |

| LINCOLN | $498,257 | $637,950 | $771,125 | $958,350 | $299,000 | $323.7 |

| MCKINLEY | $498,257 | $637,950 | $771,125 | $958,350 | $193,000 | $323.7 |

| LINCOLN | $498,257 | $637,950 | $771,125 | $958,350 | $159,000 | $323.7 |

| MINERAL | $498,257 | $637,950 | $771,125 | $958,350 | $102,000 | $323.7 |

| PERSHING | $498,257 | $637,950 | $771,125 | $958,350 | $150,000 | $323.7 |

| WHITE PINE | $498,257 | $637,950 | $771,125 | $958,350 | $120,000 | $323.7 |

| CLINTON | $498,257 | $637,950 | $771,125 | $958,350 | $155,000 | $323.7 |

| FRANKLIN | $498,257 | $637,950 | $771,125 | $958,350 | $110,000 | $323.7 |

| KINGS | $1,149,825 | $1,472,250 | $1,779,525 | $2,211,600 | $34,000 | $0.65 |

| LIVINGSTON | $498,257 | $637,950 | $771,125 | $958,350 | $230,000 | $323.7 |

| TOMPKINS | $498,257 | $637,950 | $771,125 | $958,350 | $269,000 | $323.7 |

| WASHINGTON | $498,257 | $637,950 | $771,125 | $958,350 | $250,000 | $323.7 |

| WYOMING | $498,257 | $637,950 | $771,125 | $958,350 | $139,000 | $323.7 |

| CLINTON | $498,257 | $637,950 | $771,125 | $958,350 | $165,000 | $323.7 |

| FRANKLIN | $546,250 | $699,300 | $845,300 | $1,050,500 | $475,000 | $354.9 |

| HARDIN | $498,257 | $637,950 | $771,125 | $958,350 | $130,000 | $323.7 |

| HOCKING | $546,250 | $699,300 | $845,300 | $1,050,500 | $475,000 | $354.9 |

| LICKING | $546,250 | $699,300 | $845,300 | $1,050,500 | $475,000 | $354.9 |

| LORAIN | $498,257 | $637,950 | $771,125 | $958,350 | $285,000 | $323.7 |

| MAHONING | $498,257 | $637,950 | $771,125 | $958,350 | $135,000 | $323.7 |

| MEDINA | $498,257 | $637,950 | $771,125 | $958,350 | $285,000 | $323.7 |

| MUSKINGUM | $498,257 | $637,950 | $771,125 | $958,350 | $135,000 | $323.7 |

| PAULDING | $498,257 | $637,950 | $771,125 | $958,350 | $98,000 | $323.7 |

| VINTON | $498,257 | $637,950 | $771,125 | $958,350 | $33,000 | $323.7 |

| WASHINGTON | $498,257 | $637,950 | $771,125 | $958,350 | $145,000 | $323.7 |

| BLAINE | $498,257 | $637,950 | $771,125 | $958,350 | $60,000 | $323.7 |

| GARVIN | $498,257 | $637,950 | $771,125 | $958,350 | $95,000 | $323.7 |

| KINGFISHER | $498,257 | $637,950 | $771,125 | $958,350 | $170,000 | $323.7 |

| LINCOLN | $498,257 | $637,950 | $771,125 | $958,350 | $243,000 | $323.7 |

| MCCLAIN | $498,257 | $637,950 | $771,125 | $958,350 | $243,000 | $323.7 |

| MCCURTAIN | $498,257 | $637,950 | $771,125 | $958,350 | $170,000 | $323.7 |

| MCINTOSH | $498,257 | $637,950 | $771,125 | $958,350 | $75,000 | $323.7 |

| SEMINOLE | $498,257 | $637,950 | $771,125 | $958,350 | $70,000 | $323.7 |

| WASHINGTON | $498,257 | $637,950 | $771,125 | $958,350 | $144,000 | $323.7 |

| JOSEPHINE | $498,257 | $637,950 | $771,125 | $958,350 | $360,000 | $323.7 |

| LINCOLN | $498,257 | $637,950 | $771,125 | $958,350 | $376,000 | $323.7 |

| LINN | $498,257 | $637,950 | $771,125 | $958,350 | $365,000 | $323.7 |

| WASHINGTON | $679,650 | $870,050 | $1,051,700 | $1,307,050 | $591,000 | $441.35 |

| CLINTON | $498,257 | $637,950 | $771,125 | $958,350 | $147,000 | $323.7 |

| DAUPHIN | $498,257 | $637,950 | $771,125 | $958,350 | $290,000 | $323.7 |

| FRANKLIN | $498,257 | $637,950 | $771,125 | $958,350 | $230,000 | $323.7 |

| HUNTINGDON | $498,257 | $637,950 | $771,125 | $958,350 | $120,000 | $323.7 |

| INDIANA | $498,257 | $637,950 | $771,125 | $958,350 | $114,000 | $323.7 |

| LYCOMING | $498,257 | $637,950 | $771,125 | $958,350 | $170,000 | $323.7 |

| MIFFLIN | $498,257 | $637,950 | $771,125 | $958,350 | $100,000 | $323.7 |

| WASHINGTON | $498,257 | $637,950 | $771,125 | $958,350 | $279,000 | $323.7 |

| WYOMING | $498,257 | $637,950 | $771,125 | $958,350 | $168,000 | $323.7 |

| CAROLINA | $498,257 | $637,950 | $771,125 | $958,350 | $259,000 | $323.7 |

| RINCON | $498,257 | $637,950 | $771,125 | $958,350 | $290,000 | $323.7 |

| SALINAS | $498,257 | $637,950 | $771,125 | $958,350 | $133,000 | $323.7 |

| WASHINGTON | $736,000 | $942,200 | $1,138,900 | $1,415,400 | $640,000 | $478.4 |

| ABBEVILLE | $498,257 | $637,950 | $771,125 | $958,350 | $253,000 | $323.7 |

| AIKEN | $498,257 | $637,950 | $771,125 | $958,350 | $297,000 | $323.7 |

| ALLENDALE | $498,257 | $637,950 | $771,125 | $958,350 | $60,000 | $323.7 |

| ANDERSON | $498,257 | $637,950 | $771,125 | $958,350 | $305,000 | $323.7 |

| BAMBERG | $498,257 | $637,950 | $771,125 | $958,350 | $36,000 | $323.7 |

| BARNWELL | $498,257 | $637,950 | $771,125 | $958,350 | $69,000 | $323.7 |

| BEAUFORT | $546,250 | $699,300 | $845,300 | $1,050,500 | $475,000 | $354.9 |

| BERKELEY | $586,500 | $750,800 | $907,550 | $1,127,900 | $510,000 | $380.9 |

| CALHOUN | $498,257 | $637,950 | $771,125 | $958,350 | $245,000 | $323.7 |

| CHARLESTON | $586,500 | $750,800 | $907,550 | $1,127,900 | $510,000 | $380.9 |

| CHEROKEE | $498,257 | $637,950 | $771,125 | $958,350 | $150,000 | $323.7 |

| CHESTER | $498,257 | $637,950 | $771,125 | $958,350 | $420,000 | $323.7 |

| CHESTERFIELD | $498,257 | $637,950 | $771,125 | $958,350 | $113,000 | $323.7 |

| CLARENDON | $498,257 | $637,950 | $771,125 | $958,350 | $165,000 | $323.7 |

| COLLETON | $498,257 | $637,950 | $771,125 | $958,350 | $186,000 | $323.7 |

| DARLINGTON | $498,257 | $637,950 | $771,125 | $958,350 | $180,000 | $323.7 |

| DILLON | $498,257 | $637,950 | $771,125 | $958,350 | $35,000 | $323.7 |

| DORCHESTER | $586,500 | $750,800 | $907,550 | $1,127,900 | $510,000 | $380.9 |

| EDGEFIELD | $498,257 | $637,950 | $771,125 | $958,350 | $297,000 | $323.7 |

| FAIRFIELD | $498,257 | $637,950 | $771,125 | $958,350 | $245,000 | $323.7 |

| FLORENCE | $498,257 | $637,950 | $771,125 | $958,350 | $180,000 | $323.7 |

| GEORGETOWN | $498,257 | $637,950 | $771,125 | $958,350 | $340,000 | $323.7 |

| GREENVILLE | $498,257 | $637,950 | $771,125 | $958,350 | $305,000 | $323.7 |

| GREENWOOD | $498,257 | $637,950 | $771,125 | $958,350 | $170,000 | $323.7 |

| HAMPTON | $498,257 | $637,950 | $771,125 | $958,350 | $60,000 | $323.7 |

| HORRY | $498,257 | $637,950 | $771,125 | $958,350 | $335,000 | $323.7 |

| JASPER | $546,250 | $699,300 | $845,300 | $1,050,500 | $475,000 | $354.9 |

| KERSHAW | $498,257 | $637,950 | $771,125 | $958,350 | $245,000 | $323.7 |

| LANCASTER | $498,257 | $637,950 | $771,125 | $958,350 | $420,000 | $323.7 |

| LAURENS | $498,257 | $637,950 | $771,125 | $958,350 | $305,000 | $323.7 |

| LEE | $498,257 | $637,950 | $771,125 | $958,350 | $63,000 | $323.7 |

| LEXINGTON | $498,257 | $637,950 | $771,125 | $958,350 | $245,000 | $323.7 |

| MCCORMICK | $498,257 | $637,950 | $771,125 | $958,350 | $170,000 | $323.7 |

| MARION | $498,257 | $637,950 | $771,125 | $958,350 | $122,000 | $323.7 |

| MARLBORO | $498,257 | $637,950 | $771,125 | $958,350 | $79,000 | $323.7 |

| NEWBERRY | $498,257 | $637,950 | $771,125 | $958,350 | $133,000 | $323.7 |

| OCONEE | $498,257 | $637,950 | $771,125 | $958,350 | $220,000 | $323.7 |

| ORANGEBURG | $498,257 | $637,950 | $771,125 | $958,350 | $95,000 | $323.7 |

| PICKENS | $498,257 | $637,950 | $771,125 | $958,350 | $305,000 | $323.7 |

| RICHLAND | $498,257 | $637,950 | $771,125 | $958,350 | $245,000 | $323.7 |

| SALUDA | $498,257 | $637,950 | $771,125 | $958,350 | $245,000 | $323.7 |

| SPARTANBURG | $498,257 | $637,950 | $771,125 | $958,350 | $250,000 | $323.7 |

| SUMTER | $498,257 | $637,950 | $771,125 | $958,350 | $165,000 | $323.7 |

| UNION | $498,257 | $637,950 | $771,125 | $958,350 | $69,000 | $323.7 |

| WILLIAMSBURG | $498,257 | $637,950 | $771,125 | $958,350 | $30,000 | $323.7 |

| YORK | $498,257 | $637,950 | $771,125 | $958,350 | $420,000 | $323.7 |

| BROOKINGS | $498,257 | $637,950 | $771,125 | $958,350 | $290,000 | $323.7 |

| CODINGTON | $498,257 | $637,950 | $771,125 | $958,350 | $242,000 | $323.7 |

| HAMLIN | $498,257 | $637,950 | $771,125 | $958,350 | $242,000 | $323.7 |

| HARDING | $498,257 | $637,950 | $771,125 | $958,350 | $142,000 | $323.7 |

| HUTCHINSON | $498,257 | $637,950 | $771,125 | $958,350 | $212,000 | $323.7 |

| KINGSBURY | $498,257 | $637,950 | $771,125 | $958,350 | $183,000 | $323.7 |

| LINCOLN | $498,257 | $637,950 | $771,125 | $958,350 | $352,000 | $323.7 |

| MINER | $498,257 | $637,950 | $771,125 | $958,350 | $120,000 | $323.7 |

| MINNEHAHA | $498,257 | $637,950 | $771,125 | $958,350 | $352,000 | $323.7 |

| PENNINGTON | $498,257 | $637,950 | $771,125 | $958,350 | $346,000 | $323.7 |

| PERKINS | $498,257 | $637,950 | $771,125 | $958,350 | $146,000 | $323.7 |

| SPINK | $498,257 | $637,950 | $771,125 | $958,350 | $148,000 | $323.7 |

| FRANKLIN | $498,257 | $637,950 | $771,125 | $958,350 | $232,000 | $323.7 |

| GRAINGER | $498,257 | $637,950 | $771,125 | $958,350 | $224,000 | $323.7 |

| HARDIN | $498,257 | $637,950 | $771,125 | $958,350 | $85,000 | $323.7 |

| HAWKINS | $498,257 | $637,950 | $771,125 | $958,350 | $225,000 | $323.7 |

| LINCOLN | $498,257 | $637,950 | $771,125 | $958,350 | $155,000 | $323.7 |

| MCMINN | $498,257 | $637,950 | $771,125 | $958,350 | $162,000 | $323.7 |

| WASHINGTON | $498,257 | $637,950 | $771,125 | $958,350 | $243,000 | $323.7 |

| ANGELINA | $498,257 | $637,950 | $771,125 | $958,350 | $201,000 | $323.7 |

| AUSTIN | $498,257 | $637,950 | $771,125 | $958,350 | $382,000 | $323.7 |

| COLLIN | $563,500 | $721,400 | $872,000 | $1,083,650 | $490,000 | $365.95 |

| COLLINGSWORTH | $498,257 | $637,950 | $771,125 | $958,350 | $93,000 | $323.7 |

| FANNIN | $498,257 | $637,950 | $771,125 | $958,350 | $219,000 | $323.7 |

| FRANKLIN | $498,257 | $637,950 | $771,125 | $958,350 | $189,000 | $323.7 |

| GAINES | $498,257 | $637,950 | $771,125 | $958,350 | $139,000 | $323.7 |

| HARDIN | $498,257 | $637,950 | $771,125 | $958,350 | $221,000 | $323.7 |

| HOPKINS | $498,257 | $637,950 | $771,125 | $958,350 | $250,000 | $323.7 |

| HUTCHINSON | $498,257 | $637,950 | $771,125 | $958,350 | $129,000 | $323.7 |

| KING | $498,257 | $637,950 | $771,125 | $958,350 | $34,000 | $323.7 |

| KINNEY | $498,257 | $637,950 | $771,125 | $958,350 | $302,000 | $323.7 |

| LOVING | $498,257 | $637,950 | $771,125 | $958,350 | $146,000 | $323.7 |

| MARTIN | $498,257 | $637,950 | $771,125 | $958,350 | $323,000 | $323.7 |

| MEDINA | $557,750 | $714,000 | $863,100 | $1,072,600 | $485,000 | $362.05 |

| PALO PINTO | $498,257 | $637,950 | $771,125 | $958,350 | $219,000 | $323.7 |

| RAINS | $498,257 | $637,950 | $771,125 | $958,350 | $228,000 | $323.7 |

| SABINE | $498,257 | $637,950 | $771,125 | $958,350 | $147,000 | $323.7 |

| SAN AUGUSTINE | $498,257 | $637,950 | $771,125 | $958,350 | $101,000 | $323.7 |

| SAN JACINTO | $498,257 | $637,950 | $771,125 | $958,350 | $170,000 | $323.7 |

| STERLING | $498,257 | $637,950 | $771,125 | $958,350 | $221,000 | $323.7 |

| TRINITY | $498,257 | $637,950 | $771,125 | $958,350 | $130,000 | $323.7 |

| WASHINGTON | $498,257 | $637,950 | $771,125 | $958,350 | $293,000 | $323.7 |

| WINKLER | $498,257 | $637,950 | $771,125 | $958,350 | $155,000 | $323.7 |

| UINTAH | $498,257 | $637,950 | $771,125 | $958,350 | $326,000 | $323.7 |

| WASHINGTON | $593,400 | $759,650 | $918,250 | $1,141,150 | $515,000 | $385.45 |

| ACCOMACK | $498,257 | $637,950 | $771,125 | $958,350 | $80,000 | $323.7 |

| ALBEMARLE | $545,100 | $697,800 | $843,500 | $1,048,300 | $474,000 | $354.25 |

| ALLEGHANY | $498,257 | $637,950 | $771,125 | $958,350 | $166,000 | $323.7 |

| AMELIA | $631,350 | $808,250 | $977,000 | $1,214,150 | $549,000 | $410.15 |

| AMHERST | $498,257 | $637,950 | $771,125 | $958,350 | $262,000 | $323.7 |

| APPOMATTOX | $498,257 | $637,950 | $771,125 | $958,350 | $262,000 | $323.7 |

| ARLINGTON | $1,149,825 | $1,472,250 | $1,779,525 | $2,211,600 | $72,000 | $0.65 |

| AUGUSTA | $498,257 | $637,950 | $771,125 | $958,350 | $311,000 | $323.7 |

| BATH | $498,257 | $637,950 | $771,125 | $958,350 | $113,000 | $323.7 |

| BEDFORD | $498,257 | $637,950 | $771,125 | $958,350 | $262,000 | $323.7 |

| BLAND | $498,257 | $637,950 | $771,125 | $958,350 | $132,000 | $323.7 |

| BOTETOURT | $498,257 | $637,950 | $771,125 | $958,350 | $275,000 | $323.7 |

| BRUNSWICK | $498,257 | $637,950 | $771,125 | $958,350 | $225,000 | $323.7 |

| BUCHANAN | $498,257 | $637,950 | $771,125 | $958,350 | $69,000 | $323.7 |

| BUCKINGHAM | $498,257 | $637,950 | $771,125 | $958,350 | $229,000 | $323.7 |

| CAMPBELL | $498,257 | $637,950 | $771,125 | $958,350 | $262,000 | $323.7 |

| CAROLINE | $498,257 | $637,950 | $771,125 | $958,350 | $310,000 | $323.7 |

| CARROLL | $498,257 | $637,950 | $771,125 | $958,350 | $169,000 | $323.7 |

| CHARLES CITY | $631,350 | $808,250 | $977,000 | $1,214,150 | $549,000 | $410.15 |

| CHARLOTTE | $498,257 | $637,950 | $771,125 | $958,350 | $70,000 | $323.7 |

| CHESTERFIELD | $631,350 | $808,250 | $977,000 | $1,214,150 | $549,000 | $410.15 |

| CLARKE | $1,149,825 | $1,472,250 | $1,779,525 | $2,211,600 | $72,000 | $0.65 |

| CRAIG | $498,257 | $637,950 | $771,125 | $958,350 | $275,000 | $323.7 |

| CULPEPER | $1,149,825 | $1,472,250 | $1,779,525 | $2,211,600 | $72,000 | $0.65 |

| CUMBERLAND | $498,257 | $637,950 | $771,125 | $958,350 | $234,000 | $323.7 |

| DICKENSON | $498,257 | $637,950 | $771,125 | $958,350 | $40,000 | $323.7 |

| DINWIDDIE | $631,350 | $808,250 | $977,000 | $1,214,150 | $549,000 | $410.15 |

| ESSEX | $498,257 | $637,950 | $771,125 | $958,350 | $239,000 | $323.7 |

| FAIRFAX | $1,149,825 | $1,472,250 | $1,779,525 | $2,211,600 | $72,000 | $0.65 |

| FAUQUIER | $1,149,825 | $1,472,250 | $1,779,525 | $2,211,600 | $72,000 | $0.65 |

| FLOYD | $498,257 | $637,950 | $771,125 | $958,350 | $250,000 | $323.7 |

| FLUVANNA | $545,100 | $697,800 | $843,500 | $1,048,300 | $474,000 | $354.25 |

| FRANKLIN | $498,257 | $637,950 | $771,125 | $958,350 | $275,000 | $323.7 |

| FREDERICK | $498,257 | $637,950 | $771,125 | $958,350 | $385,000 | $323.7 |

| GILES | $498,257 | $637,950 | $771,125 | $958,350 | $310,000 | $323.7 |

| GLOUCESTER | $690,000 | $883,300 | $1,067,750 | $1,326,950 | $600,000 | $448.5 |

| GOOCHLAND | $631,350 | $808,250 | $977,000 | $1,214,150 | $549,000 | $410.15 |

| GRAYSON | $498,257 | $637,950 | $771,125 | $958,350 | $130,000 | $323.7 |

| GREENE | $545,100 | $697,800 | $843,500 | $1,048,300 | $474,000 | $354.25 |

| GREENSVILLE | $498,257 | $637,950 | $771,125 | $958,350 | $167,000 | $323.7 |

| HALIFAX | $498,257 | $637,950 | $771,125 | $958,350 | $87,000 | $323.7 |

| HANOVER | $631,350 | $808,250 | $977,000 | $1,214,150 | $549,000 | $410.15 |

| HENRICO | $631,350 | $808,250 | $977,000 | $1,214,150 | $549,000 | $410.15 |

| HENRY | $498,257 | $637,950 | $771,125 | $958,350 | $82,000 | $323.7 |

| HIGHLAND | $498,257 | $637,950 | $771,125 | $958,350 | $95,000 | $323.7 |

| ISLE OF WIGHT | $690,000 | $883,300 | $1,067,750 | $1,326,950 | $600,000 | $448.5 |

| JAMES CITY | $690,000 | $883,300 | $1,067,750 | $1,326,950 | $600,000 | $448.5 |

| KING AND QUEEN | $631,350 | $808,250 | $977,000 | $1,214,150 | $549,000 | $410.15 |

| KING GEORGE | $498,257 | $637,950 | $771,125 | $958,350 | $420,000 | $323.7 |

| KING WILLIAM | $631,350 | $808,250 | $977,000 | $1,214,150 | $549,000 | $410.15 |

| LANCASTER | $498,257 | $637,950 | $771,125 | $958,350 | $255,000 | $323.7 |

| LEE | $498,257 | $637,950 | $771,125 | $958,350 | $60,000 | $323.7 |

| LOUDOUN | $1,149,825 | $1,472,250 | $1,779,525 | $2,211,600 | $72,000 | $0.65 |

| LOUISA | $498,257 | $637,950 | $771,125 | $958,350 | $332,000 | $323.7 |

| LUNENBURG | $498,257 | $637,950 | $771,125 | $958,350 | $69,000 | $323.7 |

| MADISON | $1,149,825 | $1,472,250 | $1,779,525 | $2,211,600 | $72,000 | $0.65 |

| MATHEWS | $690,000 | $883,300 | $1,067,750 | $1,326,950 | $600,000 | $448.5 |

| MECKLENBURG | $498,257 | $637,950 | $771,125 | $958,350 | $119,000 | $323.7 |

| MIDDLESEX | $498,257 | $637,950 | $771,125 | $958,350 | $345,000 | $323.7 |

| MONTGOMERY | $498,257 | $637,950 | $771,125 | $958,350 | $310,000 | $323.7 |

| NELSON | $545,100 | $697,800 | $843,500 | $1,048,300 | $474,000 | $354.25 |

| NEW KENT | $631,350 | $808,250 | $977,000 | $1,214,150 | $549,000 | $410.15 |

| NORTHAMPTON | $498,257 | $637,950 | $771,125 | $958,350 | $250,000 | $323.7 |

| NORTHUMBERLAND | $498,257 | $637,950 | $771,125 | $958,350 | $213,000 | $323.7 |

| NOTTOWAY | $498,257 | $637,950 | $771,125 | $958,350 | $169,000 | $323.7 |

| ORANGE | $498,257 | $637,950 | $771,125 | $958,350 | $349,000 | $323.7 |

| PAGE | $498,257 | $637,950 | $771,125 | $958,350 | $240,000 | $323.7 |

| PATRICK | $498,257 | $637,950 | $771,125 | $958,350 | $173,000 | $323.7 |

| PITTSYLVANIA | $498,257 | $637,950 | $771,125 | $958,350 | $108,000 | $323.7 |

| POWHATAN | $631,350 | $808,250 | $977,000 | $1,214,150 | $549,000 | $410.15 |

| PRINCE EDWARD | $498,257 | $637,950 | $771,125 | $958,350 | $165,000 | $323.7 |

| PRINCE GEORGE | $631,350 | $808,250 | $977,000 | $1,214,150 | $549,000 | $410.15 |

| PRINCE WILLIAM | $1,149,825 | $1,472,250 | $1,779,525 | $2,211,600 | $72,000 | $0.65 |

| PULASKI | $498,257 | $637,950 | $771,125 | $958,350 | $310,000 | $323.7 |

| RAPPAHANNOCK | $1,149,825 | $1,472,250 | $1,779,525 | $2,211,600 | $72,000 | $0.65 |

| RICHMOND | $498,257 | $637,950 | $771,125 | $958,350 | $97,000 | $323.7 |

| ROANOKE | $498,257 | $637,950 | $771,125 | $958,350 | $275,000 | $323.7 |

| ROCKBRIDGE | $498,257 | $637,950 | $771,125 | $958,350 | $208,000 | $323.7 |

| ROCKINGHAM | $498,257 | $637,950 | $771,125 | $958,350 | $322,000 | $323.7 |

| RUSSELL | $498,257 | $637,950 | $771,125 | $958,350 | $79,000 | $323.7 |

| SCOTT | $498,257 | $637,950 | $771,125 | $958,350 | $225,000 | $323.7 |

| SHENANDOAH | $498,257 | $637,950 | $771,125 | $958,350 | $243,000 | $323.7 |

| SMYTH | $498,257 | $637,950 | $771,125 | $958,350 | $124,000 | $323.7 |

| SOUTHAMPTON | $690,000 | $883,300 | $1,067,750 | $1,326,950 | $600,000 | $448.5 |

| SPOTSYLVANIA | $1,149,825 | $1,472,250 | $1,779,525 | $2,211,600 | $72,000 | $0.65 |

| STAFFORD | $1,149,825 | $1,472,250 | $1,779,525 | $2,211,600 | $72,000 | $0.65 |

| SURRY | $498,257 | $637,950 | $771,125 | $958,350 | $265,000 | $323.7 |

| SUSSEX | $631,350 | $808,250 | $977,000 | $1,214,150 | $549,000 | $410.15 |

| TAZEWELL | $498,257 | $637,950 | $771,125 | $958,350 | $132,000 | $323.7 |

| WARREN | $1,149,825 | $1,472,250 | $1,779,525 | $2,211,600 | $72,000 | $0.65 |

| WASHINGTON | $498,257 | $637,950 | $771,125 | $958,350 | $225,000 | $323.7 |

| WESTMORELAND | $498,257 | $637,950 | $771,125 | $958,350 | $248,000 | $323.7 |

| WISE | $498,257 | $637,950 | $771,125 | $958,350 | $100,000 | $323.7 |

| WYTHE | $498,257 | $637,950 | $771,125 | $958,350 | $187,000 | $323.7 |

| YORK | $690,000 | $883,300 | $1,067,750 | $1,326,950 | $600,000 | $448.5 |

| ALEXANDRIA CITY | $1,149,825 | $1,472,250 | $1,779,525 | $2,211,600 | $72,000 | $0.65 |

| BRISTOL CITY | $498,257 | $637,950 | $771,125 | $958,350 | $225,000 | $323.7 |

| BUENA VISTA CIT | $498,257 | $637,950 | $771,125 | $958,350 | $174,000 | $323.7 |

| CHARLOTTESVILLE | $545,100 | $697,800 | $843,500 | $1,048,300 | $474,000 | $354.25 |

| CHESAPEAKE CITY | $690,000 | $883,300 | $1,067,750 | $1,326,950 | $600,000 | $448.5 |

| COLONIAL HEIGHT | $631,350 | $808,250 | $977,000 | $1,214,150 | $549,000 | $410.15 |

| COVINGTON CITY | $498,257 | $637,950 | $771,125 | $958,350 | $99,000 | $323.7 |

| DANVILLE CITY | $498,257 | $637,950 | $771,125 | $958,350 | $108,000 | $323.7 |

| EMPORIA CITY | $498,257 | $637,950 | $771,125 | $958,350 | $168,000 | $323.7 |

| FAIRFAX CITY | $1,149,825 | $1,472,250 | $1,779,525 | $2,211,600 | $72,000 | $0.65 |

| FALLS CHURCH CI | $1,149,825 | $1,472,250 | $1,779,525 | $2,211,600 | $72,000 | $0.65 |

| FRANKLIN CITY | $690,000 | $883,300 | $1,067,750 | $1,326,950 | $600,000 | $448.5 |

| FREDERICKSBURG | $1,149,825 | $1,472,250 | $1,779,525 | $2,211,600 | $72,000 | $0.65 |

| GALAX CITY | $498,257 | $637,950 | $771,125 | $958,350 | $142,000 | $323.7 |

| HAMPTON CITY | $690,000 | $883,300 | $1,067,750 | $1,326,950 | $600,000 | $448.5 |

| HARRISONBURG CI | $498,257 | $637,950 | $771,125 | $958,350 | $322,000 | $323.7 |

| HOPEWELL CITY | $631,350 | $808,250 | $977,000 | $1,214,150 | $549,000 | $410.15 |

| LEXINGTON CITY | $498,257 | $637,950 | $771,125 | $958,350 | $403,000 | $323.7 |

| LYNCHBURG CITY | $498,257 | $637,950 | $771,125 | $958,350 | $262,000 | $323.7 |

| MANASSAS CITY | $1,149,825 | $1,472,250 | $1,779,525 | $2,211,600 | $72,000 | $0.65 |

| MANASSAS PARK C | $1,149,825 | $1,472,250 | $1,779,525 | $2,211,600 | $72,000 | $0.65 |

| MARTINSVILLE CI | $498,257 | $637,950 | $771,125 | $958,350 | $82,000 | $323.7 |

| NEWPORT NEWS CI | $690,000 | $883,300 | $1,067,750 | $1,326,950 | $600,000 | $448.5 |

| NORFOLK CITY | $690,000 | $883,300 | $1,067,750 | $1,326,950 | $600,000 | $448.5 |

| NORTON CITY | $498,257 | $637,950 | $771,125 | $958,350 | $100,000 | $323.7 |

| PETERSBURG CITY | $631,350 | $808,250 | $977,000 | $1,214,150 | $549,000 | $410.15 |

| POQUOSON CITY | $690,000 | $883,300 | $1,067,750 | $1,326,950 | $600,000 | $448.5 |

| PORTSMOUTH CITY | $690,000 | $883,300 | $1,067,750 | $1,326,950 | $600,000 | $448.5 |

| RADFORD CITY | $498,257 | $637,950 | $771,125 | $958,350 | $310,000 | $323.7 |

| RICHMOND CITY | $631,350 | $808,250 | $977,000 | $1,214,150 | $549,000 | $410.15 |

| ROANOKE CITY | $498,257 | $637,950 | $771,125 | $958,350 | $275,000 | $323.7 |

| SALEM CITY | $498,257 | $637,950 | $771,125 | $958,350 | $275,000 | $323.7 |

| STAUNTON CITY | $498,257 | $637,950 | $771,125 | $958,350 | $311,000 | $323.7 |

| SUFFOLK CITY | $690,000 | $883,300 | $1,067,750 | $1,326,950 | $600,000 | $448.5 |

| VIRGINIA BEACH | $690,000 | $883,300 | $1,067,750 | $1,326,950 | $600,000 | $448.5 |

| WAYNESBORO CITY | $498,257 | $637,950 | $771,125 | $958,350 | $311,000 | $323.7 |

| WILLIAMSBURG CI | $690,000 | $883,300 | $1,067,750 | $1,326,950 | $600,000 | $448.5 |

| WINCHESTER CITY | $498,257 | $637,950 | $771,125 | $958,350 | $385,000 | $323.7 |

| ST. CROIX ISLAN | $498,257 | $637,950 | $771,125 | $958,350 | $385,000 | $323.7 |

| ST. JOHN ISLAND | $1,059,150 | $1,355,900 | $1,639,000 | $2,036,850 | $921,000 | $0.65 |

| ST. THOMAS ISLA | $639,400 | $818,550 | $989,450 | $1,229,650 | $556,000 | $415.35 |

| BENNINGTON | $498,257 | $637,950 | $771,125 | $958,350 | $275,000 | $323.7 |

| FRANKLIN | $517,500 | $662,500 | $800,800 | $995,200 | $450,000 | $336.05 |

| WASHINGTON | $498,257 | $637,950 | $771,125 | $958,350 | $268,000 | $323.7 |

| WINDHAM | $498,257 | $637,950 | $771,125 | $958,350 | $274,000 | $323.7 |

| WINDSOR | $498,257 | $637,950 | $771,125 | $958,350 | $302,000 | $323.7 |

| ADAMS | $498,257 | $637,950 | $771,125 | $958,350 | $249,000 | $323.7 |

| ASOTIN | $498,257 | $637,950 | $771,125 | $958,350 | $316,000 | $323.7 |

| BENTON | $498,257 | $637,950 | $771,125 | $958,350 | $380,000 | $323.7 |

| CHELAN | $506,000 | $647,750 | $783,000 | $973,100 | $385,000 | $328.9 |

| CLALLAM | $498,257 | $637,950 | $771,125 | $958,350 | $400,000 | $323.7 |

| CLARK | $679,650 | $870,050 | $1,051,700 | $1,307,050 | $591,000 | $441.35 |

| COLUMBIA | $498,257 | $637,950 | $771,125 | $958,350 | $201,000 | $323.7 |

| COWLITZ | $498,257 | $637,950 | $771,125 | $958,350 | $355,000 | $323.7 |

| DOUGLAS | $506,000 | $647,750 | $783,000 | $973,100 | $385,000 | $328.9 |

| FERRY | $498,257 | $637,950 | $771,125 | $958,350 | $140,000 | $323.7 |

| FRANKLIN | $498,257 | $637,950 | $771,125 | $958,350 | $380,000 | $323.7 |

| GARFIELD | $498,257 | $637,950 | $771,125 | $958,350 | $247,000 | $323.7 |

| GRANT | $498,257 | $637,950 | $771,125 | $958,350 | $276,000 | $323.7 |

| GRAYS HARBOR | $498,257 | $637,950 | $771,125 | $958,350 | $265,000 | $323.7 |

| ISLAND | $575,000 | $736,100 | $889,800 | $1,105,800 | $435,000 | $373.75 |

| JEFFERSON | $517,500 | $662,500 | $800,800 | $995,200 | $450,000 | $336.05 |

| KING | $977,500 | $1,251,400 | $1,512,650 | $1,879,850 | $850,000 | $635.05 |

| KITSAP | $563,500 | $721,400 | $872,000 | $1,083,650 | $428,000 | $365.95 |

| KITTITAS | $498,257 | $637,950 | $771,125 | $958,350 | $390,000 | $323.7 |

| KLICKITAT | $498,257 | $637,950 | $771,125 | $958,350 | $225,000 | $323.7 |

| LEWIS | $498,257 | $637,950 | $771,125 | $958,350 | $325,000 | $323.7 |

| LINCOLN | $498,257 | $637,950 | $771,125 | $958,350 | $279,000 | $323.7 |

| MASON | $498,257 | $637,950 | $771,125 | $958,350 | $314,000 | $323.7 |

| OKANOGAN | $498,257 | $637,950 | $771,125 | $958,350 | $200,000 | $323.7 |

| PACIFIC | $498,257 | $637,950 | $771,125 | $958,350 | $250,000 | $323.7 |

| PEND OREILLE | $498,257 | $637,950 | $771,125 | $958,350 | $235,000 | $323.7 |

| PIERCE | $977,500 | $1,251,400 | $1,512,650 | $1,879,850 | $850,000 | $635.05 |

| SAN JUAN | $498,257 | $637,950 | $771,125 | $958,350 | $156,000 | $323.7 |

| SKAGIT | $545,100 | $697,800 | $843,500 | $1,048,300 | $417,000 | $354.25 |

| SKAMANIA | $679,650 | $870,050 | $1,051,700 | $1,307,050 | $591,000 | $441.35 |

| SNOHOMISH | $977,500 | $1,251,400 | $1,512,650 | $1,879,850 | $850,000 | $635.05 |

| SPOKANE | $498,257 | $637,950 | $771,125 | $958,350 | $355,000 | $323.7 |

| STEVENS | $498,257 | $637,950 | $771,125 | $958,350 | $355,000 | $323.7 |

| THURSTON | $546,250 | $699,300 | $845,300 | $1,050,500 | $435,000 | $354.9 |

| WAHKIAKUM | $498,257 | $637,950 | $771,125 | $958,350 | $305,000 | $323.7 |

| WALLA WALLA | $498,257 | $637,950 | $771,125 | $958,350 | $355,000 | $323.7 |

| WHATCOM | $603,750 | $772,900 | $934,250 | $1,161,050 | $420,000 | $391.95 |

| WHITMAN | $529,000 | $677,200 | $818,600 | $1,017,300 | $460,000 | $343.85 |

| YAKIMA | $498,257 | $637,950 | $771,125 | $958,350 | $305,000 | $323.7 |

| ADAMS | $498,257 | $637,950 | $771,125 | $958,350 | $85,000 | $323.7 |

| ASHLAND | $498,257 | $637,950 | $771,125 | $958,350 | $115,000 | $323.7 |

| BARRON | $498,257 | $637,950 | $771,125 | $958,350 | $172,000 | $323.7 |

| BAYFIELD | $498,257 | $637,950 | $771,125 | $958,350 | $150,000 | $323.7 |

| BROWN | $498,257 | $637,950 | $771,125 | $958,350 | $253,000 | $323.7 |

| BUFFALO | $498,257 | $637,950 | $771,125 | $958,350 | $156,000 | $323.7 |

| BURNETT | $498,257 | $637,950 | $771,125 | $958,350 | $150,000 | $323.7 |

| CALUMET | $498,257 | $637,950 | $771,125 | $958,350 | $255,000 | $323.7 |

| CHIPPEWA | $498,257 | $637,950 | $771,125 | $958,350 | $250,000 | $323.7 |

| CLARK | $498,257 | $637,950 | $771,125 | $958,350 | $130,000 | $323.7 |

| COLUMBIA | $498,257 | $637,950 | $771,125 | $958,350 | $400,000 | $323.7 |

| CRAWFORD | $498,257 | $637,950 | $771,125 | $958,350 | $145,000 | $323.7 |

| DANE | $498,257 | $637,950 | $771,125 | $958,350 | $400,000 | $323.7 |

| DODGE | $498,257 | $637,950 | $771,125 | $958,350 | $206,000 | $323.7 |

| DOOR | $498,257 | $637,950 | $771,125 | $958,350 | $230,000 | $323.7 |

| DOUGLAS | $498,257 | $637,950 | $771,125 | $958,350 | $200,000 | $323.7 |

| DUNN | $498,257 | $637,950 | $771,125 | $958,350 | $210,000 | $323.7 |

| EAU CLAIRE | $498,257 | $637,950 | $771,125 | $958,350 | $250,000 | $323.7 |

| FLORENCE | $498,257 | $637,950 | $771,125 | $958,350 | $110,000 | $323.7 |

| FOND DU LAC | $498,257 | $637,950 | $771,125 | $958,350 | $185,000 | $323.7 |

| FOREST | $498,257 | $637,950 | $771,125 | $958,350 | $89,000 | $323.7 |

| GRANT | $498,257 | $637,950 | $771,125 | $958,350 | $150,000 | $323.7 |

| GREEN | $498,257 | $637,950 | $771,125 | $958,350 | $400,000 | $323.7 |

| GREEN LAKE | $498,257 | $637,950 | $771,125 | $958,350 | $155,000 | $323.7 |