FHA Loans For Self-Employed Business Owners

In this article, we will cover and discuss FHA loans for self-employed business owners. If you are thinking about buying a house when you’re self-employed you need to learn about HUD self-employment guidelines. The FHA loans for self-employed borrowers might be an option for you. Below are all details ad requirements on how to get a mortgage when you are self-employed and you own a business (c-corp or s-corp).

In this article (Skip to…)

How HUD Determines Homebuyers as Self-Employed Borrowers

If you earn more than 25% of your income from a business, lenders consider you self-employed. You’ll need to provide tax returns and financial statements to prove your income. Lenders qualify you based on adjusted taxable income, not your gross income. You might need a CPA letter for the mortgage.

You might be denied for a loan if you are self-employed less than 1 year. For self-employed mortgage applicants whose tax write-offs drop their income to the point that they don’t qualify for a mortgage, there are alternatives. Some programs, for example, determine income by averaging bank statement deposits.

An underwriter may require two years’ tax returns and all schedules if the commission income is more than 25% of income in order to document the income of a commissioned borrower. Commissioned borrowers may be required to show two years’ tax returns if their commission income is more than 25% of their total income.

FHA Loans For Self-Employed Mortgage Eligibility

To qualify as a self-employed borrower, you normally need to have been in business for at least two years. But for all practical purposes, you must have been profitable for at least two years because lenders average your most recent two years of income. However, there are exceptions to the two-year rule. You might qualify with just one year of self-employment if you have at least two years of experience in the same or a similar profession. So if you had a salaried position with an employer and started a business in the same line of work, you can qualify for a home loan.

You must, however, earn at least as much in your business as you did as an employee. Some lenders will count formal training as work experience. In that case, you can count a year of schooling plus a year of employment as two years of experience. If you’ve been self-employed for less than one year, you probably won’t qualify for a home loan.

Calculating Income For FHA Loans For Self-Employed Business Owners

Many clients who want to qualify for FHA loans for self-employed applicants make the same mistake. They list their income before tax deductions on their loan application. But mortgage lenders only give you credit for taxable income (with some adjustments). So if your business brought in $10,000 a month, but you wrote off $9,000 a month in expenses, your qualifying income is not $10,000 a month. It’s $1,000 a month. Here’s a quick way to calculate an income to be approved for FHA loans for self-employed clients:

- Start with your taxable income (after deductions on your Schedule C or business tax return).

- Add back expenses that were not cash disbursements. For instance, depreciation is a tax deduction, but you don’t write someone a check for it. You can add back depletion as well.

- You can also make a case for adding back extraordinary costs that won’t be repeated. To convince a lender, you might have to supply more than two years of tax returns to prove that a cost was an isolated event. If a building went up in a wildfire, for instance, you can probably exclude that loss.

- You’ll also take out windfall income that won’t recur. So if you are not in the business of real estate investing, but your company made a killing selling off an unused building, you don’t count that as income.

You don’t have to calculate self-employment income to apply for a mortgage. Your lender will do it for you. But if you understand how lenders calculate self-employment income for a mortgage you won’t be surprised by the numbers.

FHA Loans For Self-Employed Business Owners Credit Score Requirements

- A minimum 500 credit score is required with a 10% downpayment

- For credit scores of 579+ borrowers only 3,5% down payment

- No bankruptcies in the past 2 years

- Fully documented income (past 2 years’ tax returns)

- Must be self-employed for the past 2 years if not then read how to get a mortgage without 2 years of history

How To Average Self-Employment Income

When self-employment income increases year over year, lenders average it over two years to get a monthly figure. But if your income fell, lenders will at best use the lower figure and divide by 12 to get your monthly income. And they will look closely at your business and your industry to see if the decrease is a one-time thing or a disturbing trend. If income is trending downward, a lender might discount it even more or just decline your application.

Documentation for FHA Loans For Self-Employed Mortgage Borrowers

Your documentation requirements when trying to get FHA loans for self-employed individuals are more burdensome than those of a salaried applicant. Expect to provide:

- Two years of personal tax returns

- Two years of business tax returns including schedules K-1, 1120, the 1120S

- Business License

- Year-to-date profit and loss statement (P&L)

- Balance sheet

- Signed CPA letter stating you are still in business

If the borrower doesn’t have a tax return he might use a Transcript from the IRS (which can be obtained through their portal) and an IRS tax forms 4506, 4506T, or 8821

You can prepare these documents yourself or get them from an accountant, bookkeeper, or tax preparer. Your accountant should also prepare a letter stating that your company is a going concern. That means you are in business and will continue to be in the foreseeable future. If the business is a sole proprietorship (not an LLC, partnership, or corporation), you may not have to provide business tax returns. Some lenders and programs require only one year of tax returns for highly qualified applicants. Especially if they have been in business for at least five years.

Does FHA Require 2 Years of Employment

There is no specific length of time that you need to be employed before you can qualify for an FHA loan. However, lenders will often have their own guidelines for determining whether or not an applicant is eligible for a mortgage, and these may include a minimum amount of employment history in order to demonstrate that you are able to reliably make your monthly mortgage payments.

Can I Do an FHA Cash-Out Refinance If I’m Self-employed

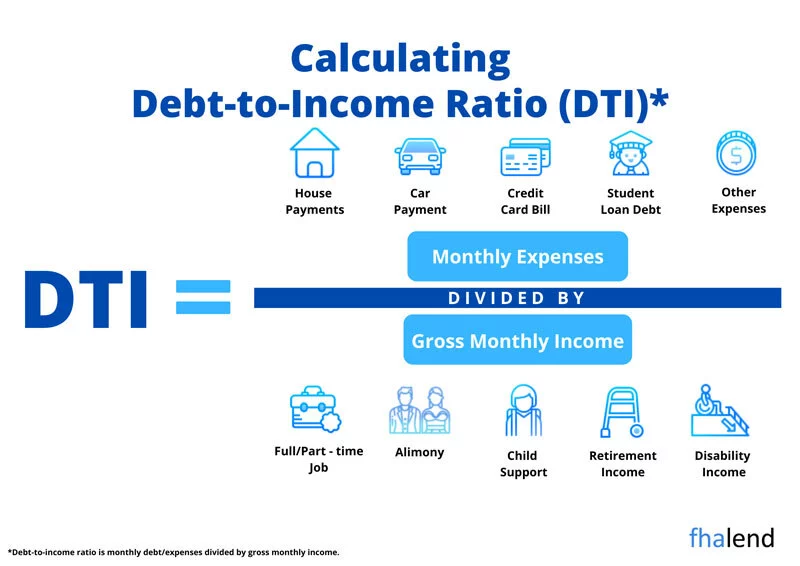

The FHA guidelines for self-employed borrowers are the same as for FHA purchases however to be able to do the FHA cash-out refinance you need to leave at least 20% of your equity in the property you would like to refinance. FHA will only allow you to borrow up to 80% of your appraised home’s value. This means that if your home is worth $100,000, you can only borrow up to $80,000 through a cash-out refinance. In addition, the FHA may require that you have a lower debt-to-income ratio if you’re self-employed. This means that your total monthly debts (including your mortgage payment) can’t exceed a certain percentage of your monthly income.

FHA Loans For Self-Employed Ownership Documents

Every FHA mortgage lender will request your documents to verify your ownership of the business in the past 2 years. Here are documents that can be requested by an underwriter

- CPA letter verifying the length of time your business was operating

- Business License

- Physical address that can be verified

- Business listing online

FHA Loans For Self-Employed Income Declined 20%

Mortgage lenders will require to provide compensating factors if your business’s income declined by 20% or more in the most recent year. Instead of AUS approval, your loan might need to go to manual underwriting which can take longer and you might need to provide additional documentation to support your loan and lower the risk for the lender.

FHA Lend Mortgage Are Experts in Helping FHA Loans For Self-Employed

Can You Amend Your Tax Returns to Qualify for FHA Loans For Self-Employed?

When you apply for a self-employed mortgage, your lender requires you to sign a form authorizing the IRS to provide income information. That IRS transcript should match the tax returns you provide to your lender. If you write off deductions very aggressively, you may have regrets when you apply for a home loan. One way of dealing with that is to amend your tax return and show more income. Surprisingly, most loan guidelines are okay with this. Another option is to take fewer write-offs at tax time and then amend your return after closing your mortgage. to take advantage of legal write-offs.

Inconsistent or Undocumented Income

If your income is not regular and reliable, you can’t use it to qualify for a mortgage. Lenders may, however, consider it a compensating factor. That said, it’s not uncommon for businesses in some industries to routinely have inconsistent income. For instance, a home builder might have a lot of expenses in Year 1 of a project. It costs money to buy property, pulls permits, and start construction.

FHA Loans For Self-Employed Borrower’s Business Profitability

The business may show big losses that year. But the next year, when the homes sell, the expenses are low and the profits are high. To prove that this is normal and that the income is reliable and ongoing, the builder might have to show the lender more tax returns — three, four, or five years of tax forms. A statement from a CPA is also helpful.

You should also prepare to explain any significant year-over-year income decrease. You do have to include income on your tax returns for lenders to count it. So your side gigs won’t help you qualify for a loan unless you’ve been at them for at least two years and have been declaring the income on your tax returns.

Bank Statement Mortgages for Self-Employed

If you can’t qualify for FHA loans for self-employed the traditional way, you may have another option. Non-QM or portfolio mortgage lenders offer an alternative product called a bank statement loan. Instead of tax returns, you supply 24 months of bank statements for your business or personal bank account. The lender averages your monthly deposits over a two-year period and comes up with a monthly figure.

This number is not usually the full average but some percentage of it. Again, if your income has dropped year over year, you’ll have some explaining to do. A good loan officer, like the professionals at FHA Lend Mortgage, can help you explain your income and determine which program will work best for you. Call us at 888 900 1020 or apply: check your eligibility.

July 3, 2022 - 7 min read