FHA Loan Limits in Mississippi | Guidelines For 2023

To find out the FHA loan limits in Mississippi and your county, you can check the below table, all limits were updated for 2023 year. Keep in mind that these are the maximum loan amounts that the FHA will insure, not the actual loans that are available. Lenders may have their own limits, which may be higher or lower than the FHA loan limit.

If you’re thinking of taking out an FHA loan in MS, it’s important to know what the FHA loan limits in Mississippi. This will help you determine whether you’re eligible for a loan and how much you can borrow. So, if you’re curious about FHA loan limits or just want to learn more about them, be sure to check out the Department of Housing and Urban Development’s website.

If you’re thinking of taking out an FHA loan in MS, it’s important to know what the FHA loan limits in Mississippi. This will help you determine whether you’re eligible for a loan and how much you can borrow. So, if you’re curious about FHA loan limits or just want to learn more about them, be sure to check out the Department of Housing and Urban Development’s website.

FHA Loan Limits in Mississippi by County For 2023

| County | Single-Family | 2 Family | 3 Family | 4 Family | Median House Price |

|---|---|---|---|---|---|

| MISSISSIPPI | $472,030 | $604,400 | $730,525 | $907,900 | $79,000 |

| MISSISSIPPI | $472,030 | $604,400 | $730,525 | $907,900 | $107,000 |

| ADAMS | $472,030 | $604,400 | $730,525 | $907,900 | $120,000 |

| ALCORN | $472,030 | $604,400 | $730,525 | $907,900 | $231,000 |

| AMITE | $472,030 | $604,400 | $730,525 | $907,900 | $108,000 |

| ATTALA | $472,030 | $604,400 | $730,525 | $907,900 | $113,000 |

| BENTON | $472,030 | $604,400 | $730,525 | $907,900 | $105,000 |

| BOLIVAR | $472,030 | $604,400 | $730,525 | $907,900 | $126,000 |

| CALHOUN | $472,030 | $604,400 | $730,525 | $907,900 | $90,000 |

| CARROLL | $472,030 | $604,400 | $730,525 | $907,900 | $119,000 |

| CHICKASAW | $472,030 | $604,400 | $730,525 | $907,900 | $89,000 |

| CHOCTAW | $472,030 | $604,400 | $730,525 | $907,900 | $228,000 |

| CLAIBORNE | $472,030 | $604,400 | $730,525 | $907,900 | $89,000 |

| CLARKE | $472,030 | $604,400 | $730,525 | $907,900 | $164,000 |

| CLAY | $472,030 | $604,400 | $730,525 | $907,900 | $123,000 |

| COAHOMA | $472,030 | $604,400 | $730,525 | $907,900 | $86,000 |

| COPIAH | $472,030 | $604,400 | $730,525 | $907,900 | $316,000 |

| COVINGTON | $472,030 | $604,400 | $730,525 | $907,900 | $244,000 |

| DESOTO | $472,030 | $604,400 | $730,525 | $907,900 | $303,000 |

| FORREST | $472,030 | $604,400 | $730,525 | $907,900 | $244,000 |

| FRANKLIN | $472,030 | $604,400 | $730,525 | $907,900 | $103,000 |

| GEORGE | $472,030 | $604,400 | $730,525 | $907,900 | $152,000 |

| GREENE | $472,030 | $604,400 | $730,525 | $907,900 | $106,000 |

| GRENADA | $472,030 | $604,400 | $730,525 | $907,900 | $137,000 |

| HANCOCK | $472,030 | $604,400 | $730,525 | $907,900 | $225,000 |

| HARRISON | $472,030 | $604,400 | $730,525 | $907,900 | $225,000 |

| HINDS | $472,030 | $604,400 | $730,525 | $907,900 | $316,000 |

| HOLMES | $472,030 | $604,400 | $730,525 | $907,900 | $316,000 |

| HUMPHREYS | $472,030 | $604,400 | $730,525 | $907,900 | $90,000 |

| ISSAQUENA | $472,030 | $604,400 | $730,525 | $907,900 | $143,000 |

| ITAWAMBA | $472,030 | $604,400 | $730,525 | $907,900 | $204,000 |

| JACKSON | $472,030 | $604,400 | $730,525 | $907,900 | $225,000 |

| JASPER | $472,030 | $604,400 | $730,525 | $907,900 | $129,000 |

| JEFFERSON | $472,030 | $604,400 | $730,525 | $907,900 | $101,000 |

| JEFFERSON DAVIS | $472,030 | $604,400 | $730,525 | $907,900 | $105,000 |

| JONES | $472,030 | $604,400 | $730,525 | $907,900 | $129,000 |

| KEMPER | $472,030 | $604,400 | $730,525 | $907,900 | $164,000 |

| LAFAYETTE | $472,030 | $604,400 | $730,525 | $907,900 | $297,000 |

| LAMAR | $472,030 | $604,400 | $730,525 | $907,900 | $244,000 |

| LAUDERDALE | $472,030 | $604,400 | $730,525 | $907,900 | $164,000 |

| LAWRENCE | $472,030 | $604,400 | $730,525 | $907,900 | $132,000 |

| LEAKE | $472,030 | $604,400 | $730,525 | $907,900 | $131,000 |

| LEE | $472,030 | $604,400 | $730,525 | $907,900 | $204,000 |

| LEFLORE | $472,030 | $604,400 | $730,525 | $907,900 | $119,000 |

| LINCOLN | $472,030 | $604,400 | $730,525 | $907,900 | $183,000 |

| LOWNDES | $472,030 | $604,400 | $730,525 | $907,900 | $200,000 |

| MADISON | $472,030 | $604,400 | $730,525 | $907,900 | $316,000 |

| MARION | $472,030 | $604,400 | $730,525 | $907,900 | $120,000 |

| MARSHALL | $472,030 | $604,400 | $730,525 | $907,900 | $303,000 |

| MONROE | $472,030 | $604,400 | $730,525 | $907,900 | $126,000 |

| MONTGOMERY | $472,030 | $604,400 | $730,525 | $907,900 | $111,000 |

| NESHOBA | $472,030 | $604,400 | $730,525 | $907,900 | $106,000 |

| NEWTON | $472,030 | $604,400 | $730,525 | $907,900 | $110,000 |

| NOXUBEE | $472,030 | $604,400 | $730,525 | $907,900 | $85,000 |

| OKTIBBEHA | $472,030 | $604,400 | $730,525 | $907,900 | $248,000 |

| PANOLA | $472,030 | $604,400 | $730,525 | $907,900 | $105,000 |

| PEARL RIVER | $472,030 | $604,400 | $730,525 | $907,900 | $196,000 |

| PERRY | $472,030 | $604,400 | $730,525 | $907,900 | $244,000 |

| PIKE | $472,030 | $604,400 | $730,525 | $907,900 | $158,000 |

| PONTOTOC | $472,030 | $604,400 | $730,525 | $907,900 | $204,000 |

| PRENTISS | $472,030 | $604,400 | $730,525 | $907,900 | $204,000 |

| QUITMAN | $472,030 | $604,400 | $730,525 | $907,900 | $69,000 |

| RANKIN | $472,030 | $604,400 | $730,525 | $907,900 | $316,000 |

| SCOTT | $472,030 | $604,400 | $730,525 | $907,900 | $134,000 |

| SHARKEY | $472,030 | $604,400 | $730,525 | $907,900 | $81,000 |

| SIMPSON | $472,030 | $604,400 | $730,525 | $907,900 | $316,000 |

| SMITH | $472,030 | $604,400 | $730,525 | $907,900 | $138,000 |

| STONE | $472,030 | $604,400 | $730,525 | $907,900 | $225,000 |

| SUNFLOWER | $472,030 | $604,400 | $730,525 | $907,900 | $110,000 |

| TALLAHATCHIE | $472,030 | $604,400 | $730,525 | $907,900 | $88,000 |

| TATE | $472,030 | $604,400 | $730,525 | $907,900 | $303,000 |

| TIPPAH | $472,030 | $604,400 | $730,525 | $907,900 | $113,000 |

| TISHOMINGO | $472,030 | $604,400 | $730,525 | $907,900 | $123,000 |

| TUNICA | $472,030 | $604,400 | $730,525 | $907,900 | $303,000 |

| UNION | $472,030 | $604,400 | $730,525 | $907,900 | $143,000 |

| WALTHALL | $472,030 | $604,400 | $730,525 | $907,900 | $159,000 |

| WARREN | $472,030 | $604,400 | $730,525 | $907,900 | $169,000 |

| WASHINGTON | $472,030 | $604,400 | $730,525 | $907,900 | $103,000 |

| WAYNE | $472,030 | $604,400 | $730,525 | $907,900 | $100,000 |

| WEBSTER | $472,030 | $604,400 | $730,525 | $907,900 | $248,000 |

| WILKINSON | $472,030 | $604,400 | $730,525 | $907,900 | $90,000 |

| WINSTON | $472,030 | $604,400 | $730,525 | $907,900 | $123,000 |

| YALOBUSHA | $472,030 | $604,400 | $730,525 | $907,900 | $109,000 |

| YAZOO | $472,030 | $604,400 | $730,525 | $907,900 | $316,000 |

Maximum FHA Loan Amount When Applying in Mississippi?

Estimating FHA loan limits can seem tricky, but it’s not as difficult as you might think. There are a few important things to keep in mind when estimating the amount you may be able to borrow with an FHA loan.

- The first step is to determine the maximum mortgage limit for your county. This information is available from the Department of Housing and Urban Development (HUD) on their website.

- Once you have determined the maximum mortgage limit for your county, you will need to subtract the down payment amount from this limit. This will give you the maximum loan amount that you are eligible for.

- Keep in mind that the FHA loan limits vary depending on the type of property being financed. The limits are higher for multi-unit properties and lower for single-family homes.

- It’s also important to note that these limits are subject to change, so be sure to check with HUD periodically to make sure you have the most up-to-date information.

Now that you know how to estimate FHA loan limits, you can start the process of applying for a loan. Be sure to consult with a lender to find out if an FHA loan is the right option for you.

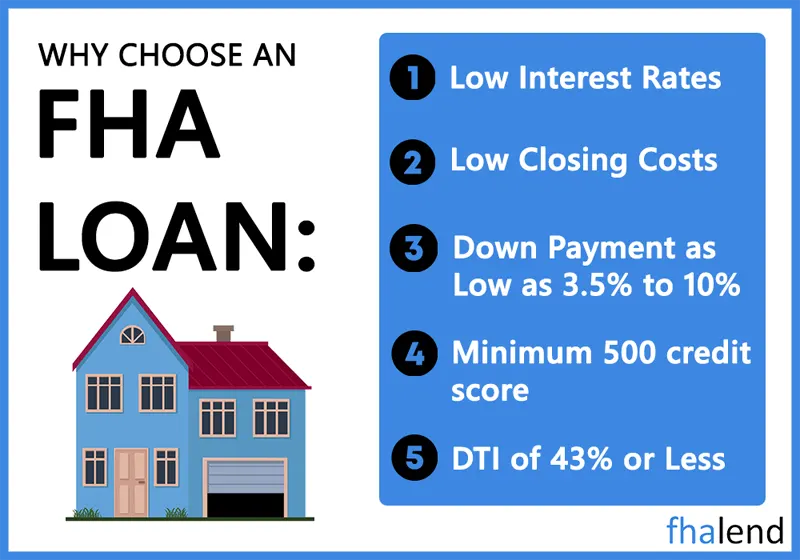

When it comes to home buying, there are a variety of loan options available. Among the most popular types of loans is the Federal Housing Administration (FHA) loan. This type of loan has been around since 1934 and is insured by the federal government. Here are six things to keep in mind when applying for an FHA loan:

Your credit score must be at least 580 to qualify for an FHA loan.

- When it comes to getting a mortgage, the credit score requirements for FHA loans are much more forgiving than traditional mortgages. In most cases, borrowers can have a credit score as low as 580 and still be approved for an FHA loan. This is because the FHA is backed by the federal government, so lenders know that they are less likely to lose money on a loan that is backed by the FHA.

- However, just because you qualify for an FHA loan doesn’t mean that you should necessarily get one. There are a few things to consider before applying for an FHA loan, such as whether you plan to stay in your home long-term or sell it soon after buying it.

- If you are interested in learning more about credit score requirements for FHA loans, or if you would like to get pre-approved for an FHA loan, please give us a call. We would be happy to help you!

You must have a debt-to-income ratio of 50% or less.

- The good news is that there are many loan options available, including those backed by the Federal Housing Administration, or FHA. The FHA has looser eligibility requirements than most other lenders, making it a great option for those with a lower credit score or who have struggled to save for a down payment.

- However, even with an FHA loan, you will still need to meet certain DTI requirements. These requirements vary depending on the type of loan you choose, but typically your DTI cannot exceed 43%. This means that your total monthly debt payments, including your mortgage, cannot exceed 43% of your monthly income.

Your mortgage payment cannot exceed 29% of your monthly income.

- The Department of Housing and Urban Development (HUD) has specific requirements for the loan-to-value (LTV) ratio on Federal Housing Administration (FHA) mortgages. In order to be eligible for an FHA mortgage, the property must have an LTV ratio of no more than 96.5 percent.

- This means that the mortgage amount cannot exceed 96.5 percent of the property’s value.

- There are several ways to calculate the LTV ratio. The most common method is to divide the loan amount by the property’s value.

- Another way to calculate the LTV ratio is to divide the loan amount by the purchase price plus closing costs. HUD takes into account both of these methods when determining whether a property meets its LTV requirements.

- There are a few exceptions to the LTV requirement. For example, if the property is being used as a primary residence, the LTV ratio can be as high as 97.75 percent. And, in some cases, the LTV ratio can be higher if the property is being refinanced.

You must have at least a 3.5% down payment.

- When it comes to down payment requirements for an FHA loan, there are a few things that borrowers need to know.

- For one thing, the minimum down payment for an FHA loan is just 3.5%. That’s significantly lower than the typical 20% down payment required by most lenders. And, even better, there are a number of ways that you can come up with that down payment.

- One option is to use cash that you have on hand. Another option is to get a gift from a friend or family member. You can also use money from a retirement account or sell assets like stocks or bonds. And if you have difficulty coming up with the full 3.5%, you may be able to use a down payment assistance program.

- Whatever your situation, it’s important to know that FHA loans offer a number of advantages.

- For one thing, they have more flexible credit requirements than most other types of loans.

- They also come with low-interest rates, and government backing can make them easier to qualify for. So if you’re interested in buying a home but don’t have a large down payment saved up, an FHA loan may be the perfect option for you.

You must live in the home you’re buying.

- When it comes to home buying, the Federal Housing Administration (FHA) is one of the most popular mortgage lenders. They offer a range of loan products, including mortgages that are backed by the government. One of the things that make FHA loans in Mississippi so popular is their relaxed occupancy requirements.

- Borrowers aren’t required to live in the home they purchase with an FHA loan.

- This is a big plus for people who are looking for a vacation home or investment property. It also opens up homeownership opportunities for people who may not be able to meet traditional occupancy requirements.

- There are a few things borrowers need to know about FHA occupancy requirements before they apply for a loan. For example, the property must be used as the borrower’s principal residence within 60 days of the loan closing. And, if the property is not used as the borrower’s principal residence, the mortgage must be insured by the FHA.

- Borrowers should also be aware that they are responsible for meeting all HUD requirements, even if they don’t live in the home. This includes maintaining the property and keeping it in good condition.

FHA loans are available for both purchase and refinance transactions.

- You can also refinance your FHA loan with an FHA streamline refinance or do a cash-out refinance on a property to withdraw some money (the program is really popular now because houses in most places in Mississippi appreciated in past few years.)

FHA Loan Limits in Mississippi for 203k Rehab Loan

The most important requirement is that the property being financed must be used as the borrower’s principal residence. The loan cannot be used to purchase a second home or investment property. In addition, the maximum mortgage amount that can be borrowed is based on the lesser of the sale price or appraised value of the property.

Borrowers must also meet income requirements in order to qualify for a 203k loan. The total monthly housing expense – including mortgage payments, taxes, insurance, and any other applicable fees – cannot exceed 31% of the borrower’s monthly gross income. Additionally, the total debt burden – including the new mortgage and all existing debts – cannot exceed 43% of the borrower’s monthly gross income.

Borrowers must also meet income requirements in order to qualify for a 203k loan. The total monthly housing expense – including mortgage payments, taxes, insurance, and any other applicable fees – cannot exceed 31% of the borrower’s monthly gross income. Additionally, the total debt burden – including the new mortgage and all existing debts – cannot exceed 43% of the borrower’s monthly gross income.

There are also some property requirements that must be met. The home must be in good condition and meet minimum property standards as defined by HUD. The property must also be eligible for FHA financing. You need to also remember that within 90 days from the day you closed on your property you cannot sell it (a flipping rule by HUD).

Finally, borrowers must go through a 203k loan approval process in order to ensure they meet all the requirements. This includes a credit check, an appraisal of the property, and verification of employment and income

Mississippi Down Payment Assistance Program

The Mississippi Home Corporation (MHC) has two distinct mortgage programs, each with its own variety of down payment assistance.

- Smart6: A 30-year fixed mortgage with a $6,000 down payment and 0% interest that matures when you sell the property.

- MRB7: After 10 years, the borrower may choose to have $7,000 of the down payment assistance forgiven.

For first-time homebuyers (including those who haven’t owned a house in the previous three years), the MRB7 is restricted to first-timers, while Smart6 can be utilized by both first-time and repeat buyers.

Visit the MHC’s website for additional information. Check out HUD’s list of other Mississippi homeownership financial assistance programs, as well.